Equities

Quarterly Equities and Multi Asset Outlook - Q2 2023

20 min read 13 Apr 23

When you cannot predict, prepare

- In the current market backdrop, two drivers matter for markets: the forthcoming central bank decisions, and the likelihood, timing and depth of a recession.

- While the direction of datapoints may be relatively easy to infer, the timing, pace and extent are far more difficult to pinpoint.

- When we cannot predict, we must prepare: we need to assess the various possible scenarios that could influence market behaviour, and be prepared to take advantage of opportunities while minimising the impact of risk.

The resilience of markets, particularly equities, has surprised many. Such resilience could persist in the months ahead, albeit not without bouts of volatility. At a broad index level, equity and fixed income valuations appear to be accurately reflecting the risks and opportunities presented by the current macroeconomic backdrop, but pockets of mispricing are occurring at a more granular level, creating opportunities for active investors. We are finding attractive opportunities in Emerging Market (EM) sovereigns, Investment Grade (IG) credit, high-quality cyclical stocks and Asian equities in particular. We maintain our stance that this is not a market for ‘broad strokes investing’, rather one where selection is the main driver of alpha, diversification is key and volatility has to necessarily become our friend.

To read the note in full, please click 2023 Equities & Multi Asset Outlook

- CIO Outlook

- Multi Asset

- Global

- UK

- Japan

- Asia Pacific ex Japan

- Emerging Markets

- Impact

- Equity Research

- Convertibles

Fabiana Fedeli,

Chief Investment Officer,

Equities, Multi Asset and Sustainability

Our ultimate job as asset managers is not to make perfect macroeconomic predictions. Rather, it is to make sure that we preserve and grow the capital that our clients entrust us with, responsibly. If this comes on the back of having accurately forecasted US CPI to be 6.0% rather than 6.1%, that’s great foresight and most likely also a bit of luck. In reality, more often than not, the secret sauce is in determining the odds of the various possible scenarios that could influence market behaviour, understanding if these are priced in or may drive wider moves, and making sure that the portfolio is prepared to take advantage of opportunities and minimise the impact of risks.

This approach is even more relevant in a market such as the one we are experiencing now, where predictions are extremely difficult to ace. The direction of data (declining inflation and slowing demand) may be relatively easy to infer, but the timing, pace and extent of the moves, and whether these will occur in a straight line or (more likely) two steps forward and one, maybe two, backwards, is far more difficult to pinpoint. And when we cannot predict, we should most definitely prepare.

When we published our last Quarterly Equities and Multi Asset Outlook, in early January, our title ‘Expected Surprises in 2023’ was predicated on the fact that after a global pandemic and a war in Europe, we have learnt to shift our mindset from ‘what should we expect ahead’ to ‘what are we not expecting ahead and, hence, unprepared for’. We argued that the complexity of the macroeconomic backdrop brings with it both upside and downside risks and, while the fixed income market appeared better positioned than the equity market in the event of a meaningful recession, with expectations of a recession being increasingly entrenched – particularly in Europe – a milderthan-expected outcome could be an unexpected bonus that would propel equities higher. We concluded by saying that whatever 2023 had in store, we were expecting surprises.

And surprises we had. These included the circumstances surrounding the collapse of four banks; the wide swings in rate expectations that ensued; and the resilience, not to mention the outperformance, of equities vis-à-vis fixed income.

The collapse, within quick succession, of Silicon Valley Bank (SVB), Silvergate, Signature and Credit Suisse is most likely going to become the subject of infinite business school case studies. We all thought that a credit crisis a la 2008, with a series of connected credit events, was a clear risk in the future. That said, it was relegated to the tails of the risk distribution curve and considered as the most extreme and feared recession scenario, which would – yet again – undermine trust in the financial system for a protracted period of time. But the bank failures that we witnessed in March were not the start of a systemic credit event (or at least it does not appear to be the case as of now), but rather the product of idiosyncratic issues. These incidents were quickly ring-fenced by regulators and central banks, with limited impact on the collective trust in the broader global financial system. Although concerns around regional US banks and smaller financial institutions are likely to persist.

And for those who, at the end of 2022, put great effort into forecasting what central banks would do three months into the future, the first quarter of 2023 delivered a memorable lesson. The expectations of the Fed Future Implied Rates swung by 120 basis points (bps) between 28 February 2023 and 24 March 2023, and even the less exciting European Central Bank (ECB) saw the Overnight Index Swaps Implied Rates move by more than 66bps. But the wide range of moves wouldn’t have been quite as impressive if they hadn’t been accompanied by erratic changes in direction: down in January, up in February, down in March.

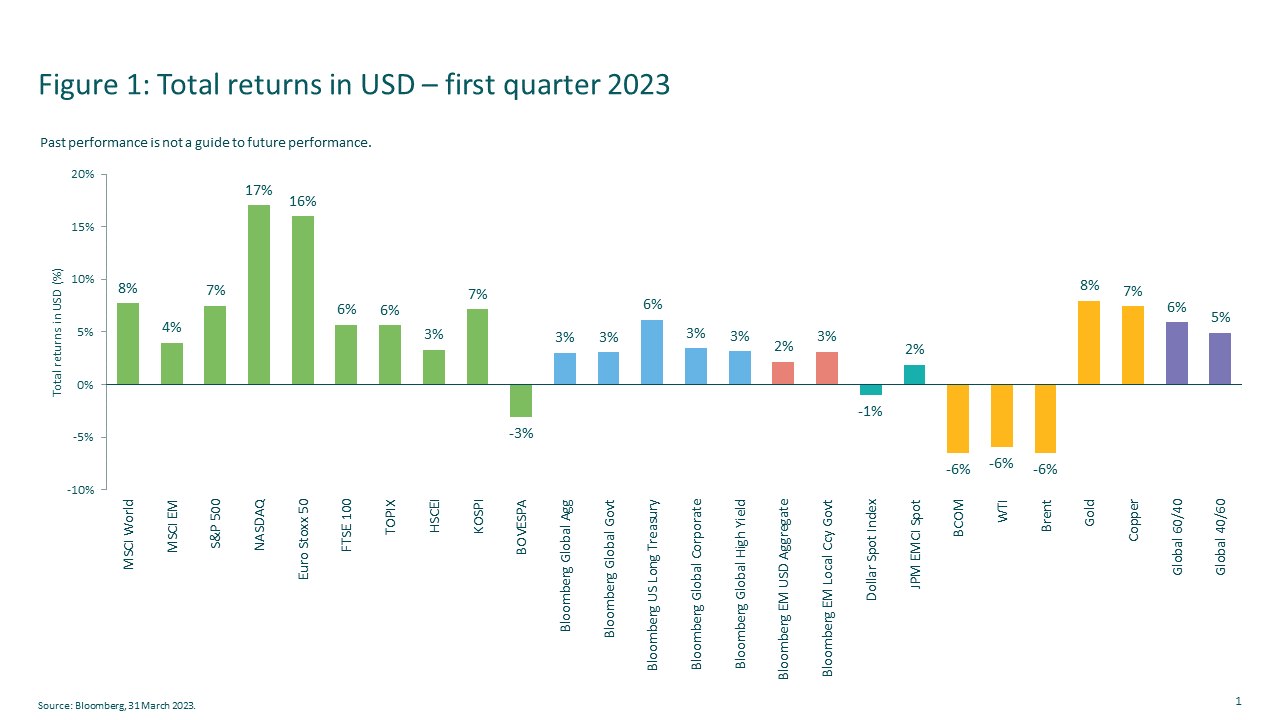

In all of this, equity markets – which looked less attractive than their fixed income equivalents earlier this year, after a glorious January, a torrid February (and first half of March), and a decisive recoup in late March – took the gold medal for resilience (Figure 1).

What is more noticeable is that, with the exception of some short periods of volatility, both equity and credit markets appeared to behave reasonably rationally. Banks, and in particular regional US banks, took the brunt of the sell-off, while other sectors remained relatively resilient, and delivered differentiated performance. However, sector returns at an aggregate level belied greater return dispersion within sectors, creating opportunities for those willing to dig deeper into the fundamentals of single stock and credit names.

What does this mean for what lies ahead and how are we preparing our portfolios?

The market remains data driven and volatile, exacerbated by the increased volumes of short-dated derivatives. Behind all that noise though there are, ultimately, two key drivers that matter for markets: i) forthcoming central bank decisions (and any datapoints that can support the direction of travel in either direction), and ii) the likelihood, timing and depth of a recession. However, on both counts, while we can guess the direction of travel, the timing and intermediate steps are far from certain.

Central bank tightening should be close to the end, but we are still uncertain on when that end will come. In our last Quarterly, we stated that central banks were likely to stop hiking sometime in the first half of 2023. This is still possible, particularly as the woes of the banking sector in the US are likely to have some negative impact on the ability and/or willingness of financial institutions to lend – doing some of the liquidity tightening work for central banks. The market still expects the Fed to cut from the second half of the year, which has continued to support equity markets. I fail to see the likelihood of rate cuts happening this year. If I am wrong, and cuts were to occur, it would spell bad news for risk assets – starting with equities – as they would most likely be triggered by a meaningful recession, which is not our base case scenario. The other trigger for a cut, inflation declining to at or below 2% later this year, appears even more unlikely.

And when it comes to the other key market driver, ie, the likelihood, timing and depth of a recession, we are even more in the dark – or, at most, we only have a glimmering speck of light. Over the past month, we have seen a number of activity-related datapoints, globally, either remain weak or deteriorate, and there is a high likelihood that we will be facing further deterioration in demand. However, the timing and the extent of a recession remains uncertain at this point. One of those ‘known unknowns’. Let’s not forget that recessions can come with a lag. Looking at US data of recessions that appear triggered by a rate hike cycle from 1965 to date, recessions appear to occur to varying degrees and can appear with a wide range of lags of between five and 15 months from the last rate hike. Some recessions, like in the 1970s, started before the Fed ended its tightening, but the extent of hikes in the 1970s were much higher (960 bps and 1300 bps respectively in each successive recession period) than the expected terminal rates for this hiking cycle. Possibly the 540 bps of rate hikes between July 1967 and August 1969 were the closest to current times, headline inflation rose to 6% and the recession only started in January 1970 with a mild (-0.6%) GDP contraction. But, while history may rhyme, it doesn’t necessarily repeat itself. Market performance, and particularly the relative performance of equities versus fixed income markets, will hinge on the length and depth of a slowdown versus current expectations.

So, we are none the wiser on what awaits us ahead. Hence, we need to be prepared for the range of likely outcomes.

We maintain our stance that this is not a market for ‘broad strokes investing’ (taking directional macroeconomic calls and swinging entire portfolios one way or the other). The market remains one where selection is the main driver of alpha, diversification is key and volatility has to necessarily become our friend.

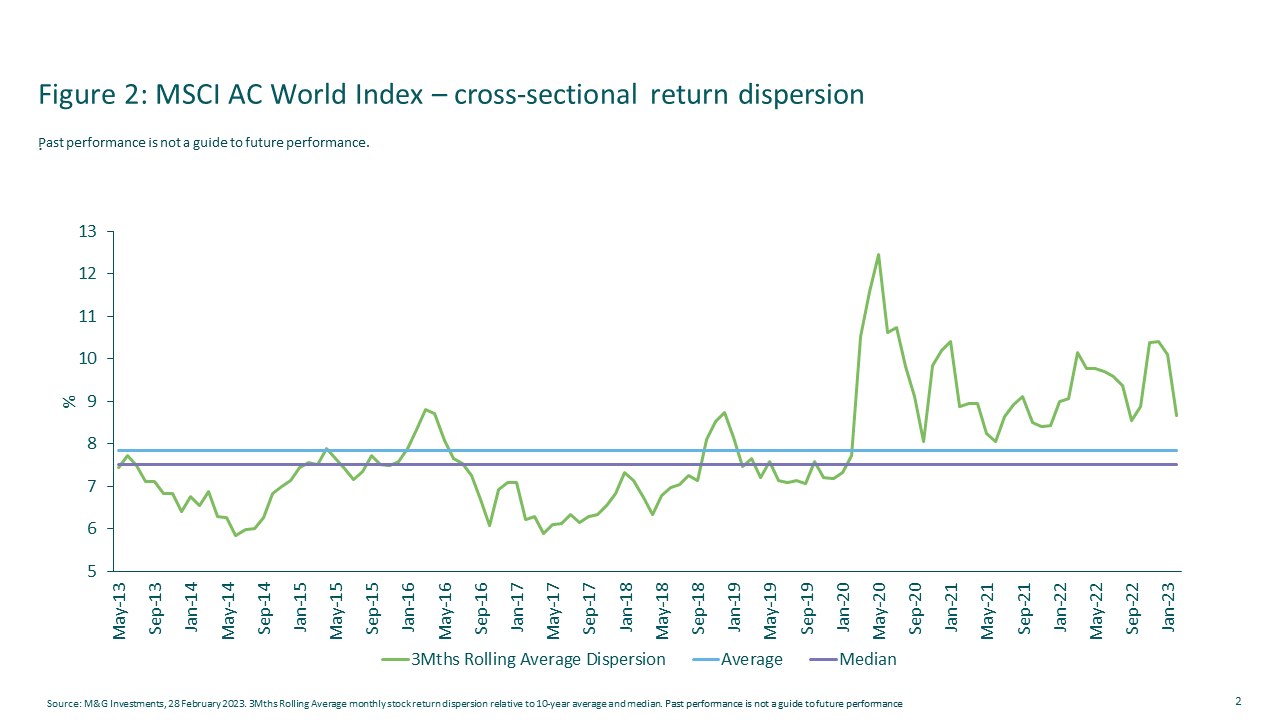

We remain focused on bottom up, differentiated research, rather than aspire to answer big macroeconomic questions. The market looks to be rewarding such an approach. Figure 2 shows how the dispersion of returns of stocks in the MSCI AC World Index have been trending above their 10-year average and median.

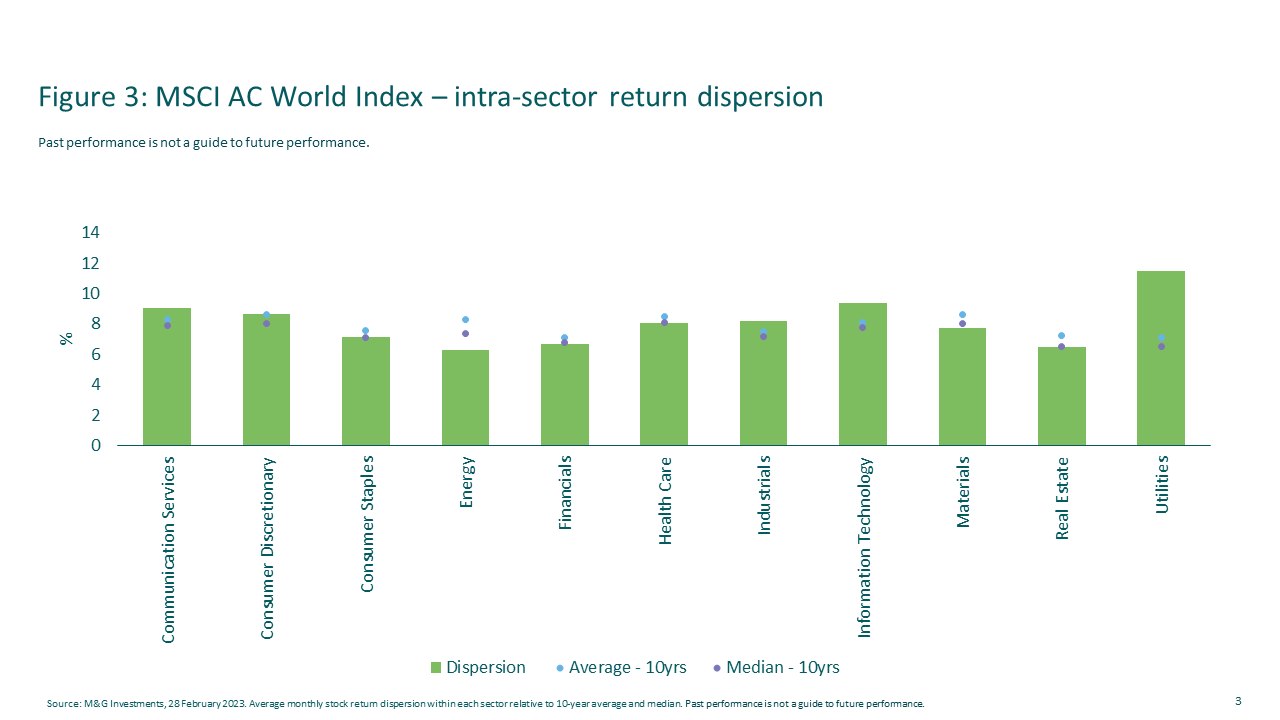

This is not only true between sectors, but, as shown in Figure 3, in a number of cases also within sectors – where the dispersion of returns between stocks in a number of sectors is trending above the 10-year average and median, meaning that investors are making a distinction between companies with weaker and stronger prospects.

In our opinion, while at a broad index level equity and fixed income valuations appear to be accurately reflecting the set of risks and opportunities presented by the current macroeconomic backdrop, the pockets of mispricing are occurring at a more granular level. Think of the share price drop in financials around the world in March. The safer and more risky were victims of the same fate, offering a good opportunity for active managers to shop for investments in some high-quality financial institutions.

In line with our belief in maintaining diversified portfolios, where selection is the key alpha driver and we stand ready to take advantage of tactical opportunities, our multi asset portfolios continue to hover around a neutral stance between equities and fixed income, and trade tactically around those positions, putting more focus on the underlying composition of the portfolios. More recently, we have taken some profit from equities, moving to a small underweight. Within equities, we maintain our relative preference for non-US markets, where we find more compelling opportunities from a valuations vis-à-vis earnings profile standpoint.

In fixed income, our multi asset strategies have moved to a neutral duration position from a small overweight. We did so by scaling back on the long end of the Treasuries curve after the recent rally. We also continue to like selected emerging market sovereigns and currencies, such as Brazil and Mexico. Elsewhere, we have been taking advantage of some opportunities in terms of both spread and outright duration exposure in areas of European Investment Grade credit across our Sustainable and Income strategies.

Across many of our portfolios, both in multi asset and in equities, we maintain higher-than-average levels of cash to take advantage of tactical opportunities.

Within equities, we have sold out of some more defensive names that had performed well in recent weeks. We took advantage of the market volatility to buy into higher-quality cyclicals, including large banks. These have strong credit and liquidity profiles, are tightly regulated, and yet saw a significant price drop amid recent events in the US and Switzerland. From a country standpoint, we continue to find compelling opportunities in Japan, where a new datapoint is providing a further catalyst. Japan has been one of our favourite markets, as we have found a number of companies that are improving operational leverage with a positive impact on earnings growth, alongside increasing shareholder returns via raising dividends and share buybacks, even without the support of the macroeconomic backdrop.

However, there may indeed be an emerging macroeconomic tailwind. Japan’s unions recently secured significant increases in this year’s shunto pay-bargaining round; the mean increase appears to be in the region of 4%, above market expectations and driven by labour shortages. According to our Japan investment team, this could be the trigger for the domestic economy to start experiencing some self-sustaining growth in the years ahead, as consumption responds to higher wages. Importantly, we believe that corporate profit margins will be able to offset the negative impact of higher wage costs given the gains in productivity that we have already started to see in the corporate sector and some transfer on pricing. This does not appear to be on the radar screen for most investors.

We also continue to find opportunities in China. Our Asia and Emerging Market (EM) portfolios added core China holdings early in the fourth quarter of 2022, when sentiment was especially poor around all things China. More recently, we reduced exposure to perceived China re-opening ‘winners’, which had rallied aggressively, and allocated resources to longterm structural growth areas, which fell out of favour, like certain renewable energy companies.

We have witnessed some unexpected events in the first quarter of 2023.

Above all, the resilience of markets, particularly equities, has surprised many. Such resilience could persist in the months ahead, albeit not without bouts of volatility. We are, however, not out of the woods yet, and a number of risks could materialise and spoil the party: higher inflation (helped by the recent OPEC+ output cuts), an earlier-than-expected and deeper-than-expected slowdown in demand, and further woes in the financial sector. In the age of 24/7 mobile banking (which in the last quarter allowed c. 25% of deposits to take flight at two institutions within a day), a breakdown of trust in the financial system and a ‘run on’ deposits could bring down even the strongest bank. Anything is possible but offering clear predictions at this point is a futile exercise. In our opinion, a far smarter choice is to prepare.

In the following pages, you will find views and insights from our Multi Asset and Equities teams, as well as an overview from our Global Banks analyst, offering more colour at a regional or thematic level. We wish you an enjoyable and – hopefully – interesting read, and a successful second quarter ahead.

Steven Andrew,

Fund Manager, Multi Asset

Liquidity tightening doing the heavy lifting from here?

The opening months of 2023 brought with them a sharp reminder of the capacity for financial markets to be surprised.

The air of cautious optimism that had accompanied a rally across all major asset classes in January had been gradually replaced through February with increased circumspection around the market’s favourite topic: US interest rate policy. In this vein, the Federal Open Market Committee’s (FOMC) 25 basis points (bps) February rate hike was received as a hawkish signal, as the accompanying statement warned that ‘ongoing increases in the target range will be appropriate’. After this, stronger-than-expected economic data, most notably from the labour market, served to encourage markets to price-in rates continuing to rise into the second half of the year, peaking beyond 5.5%.

As recently as 9 March 2023, Federal Reserve (Fed) Chairman Jerome Powell sharpened the hawkish tone further, stating that ‘the latest economic data have come in stronger than expected, which suggests that the ultimate level of interest rates is likely to be higher than previously anticipated.’

The following day, everything changed.

Markets are now priced for the next move in US interest rates to be down.

The collapse of Silicon Valley Bank (SVB) and the ensuing exploration of contagion fears has overwhelmed any indicators from the real economy that the Fed might still have some work to do. Indeed, the effective tightening in liquidity provision likely to be offered by a newly-cautious banking sector is now perceived as doing the heavy lifting from here, with short-run macro data seen as categorically backward-looking and less relevant.

As asset allocators, we are used to the market’s occasional reminder that it is more than ready to teach humility to any over-confident, prediction-laden investors. So it is with a healthy lack of certainty that we confront the range of plausible routes down which the global economy and markets may now travel. Observing market price behaviour is a key starting point.

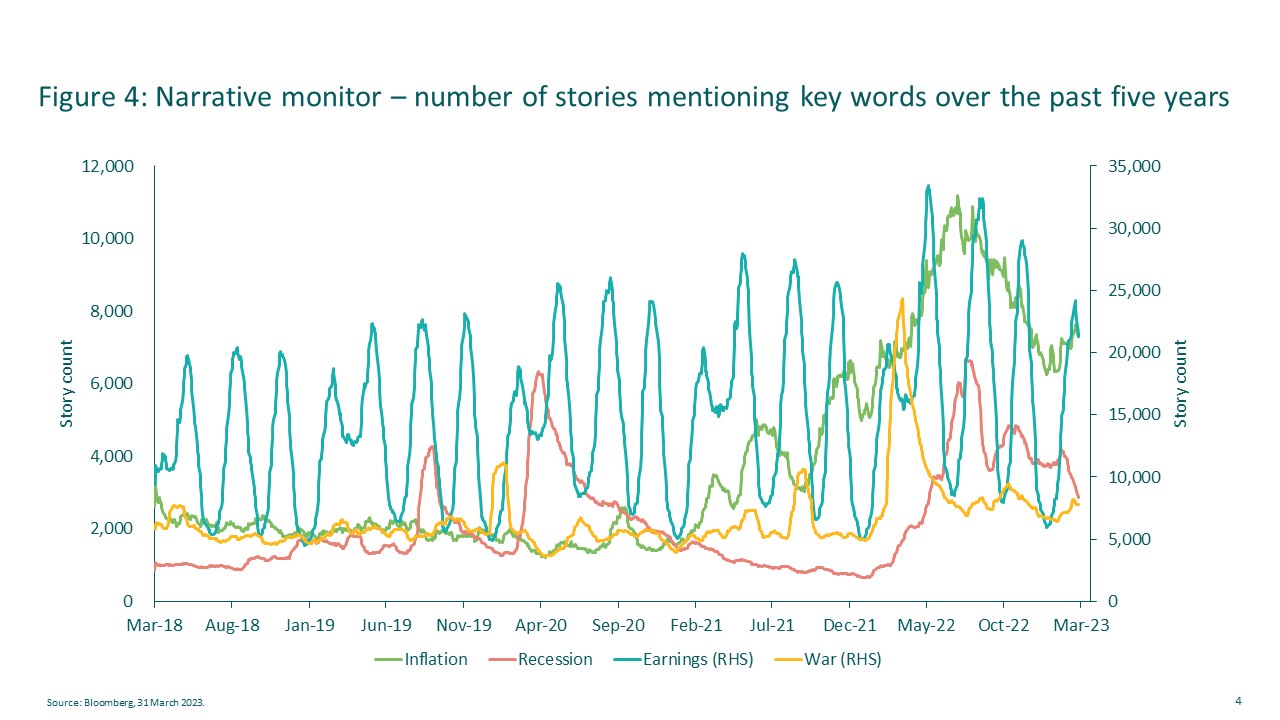

In the context of such a sharp reappraisal of the policy-rate path, it is interesting to note that the overall equity market continues to be relatively well behaved (substantially supported in the US by large cap tech which may be perceived as being somewhat ahead of the game). Furthermore, an almost too-composed response to events by financial markets at large is illustrated by our investor ‘narrative monitor’, which is showing no meaningful change in the level of stated concerns about recession (or inflation) in market news media, despite what can reasonably be considered a meaningful upset.

As we have seen in the past few weeks, with the European Central Bank (ECB) hiking 50 bps and the Fed hiking 25 bps, central banks remain primarily focused on inflation-fighting. In this regard, it will be important to assess signals from the credit channel that the banking crisis may indeed be ‘helping’.

The strong move in bonds, with long-term treasuries rallying from 4.0% to about 3.6%, delivering a capital gain of more than 5.0% over a matter of days, has led us to tactically scale-back our duration exposure, taking profit from such an outsized price move.

More strategically, we continue to see enhanced return and diversification opportunities across the fixed income space – as demonstrated by the renewed decorrelation seen across asset classes in recent weeks. We maintain a preference for the long end of the Treasuries curve (though much reduced from the fourth quarter of 2022) and we also like selected emerging market sovereigns and currencies, such as Brazil and Mexico. Within credit, we have been taking advantage of some interesting opportunities in terms of both spread and outright duration exposure in areas of European Investment Grade credit across our Sustainable and Income strategies. For our broader Multi Asset range, we maintain a relatively neutral stance on credit overall. Elsewhere, our equity exposure is neutral to underweight, and we have a relative preference for non-US markets. Having responded to market volatility in the fourth quarter, we have generally been moving to more neutral positions in our strategies, with scope to add risk should ‘episodes’ of volatility present opportunities.

Daniel White,

Head of Global Equities

Recent events are a helpful reminder that financial markets are full of uncertainties

We continue to observe a rapidly-evolving macroeconomic environment. We are about 12 months into an aggressive rate-hike cycle, and the lagged effects are starting to manifest themselves. The impact on US regional banks’ balance sheets being one. Our exposure is relatively neutral now within the equity space, with a preference for cheaper markets, some large banks and technology. Technology might benefit from easing rates pressure and robust, cash-rich business models (just reinforced by recent cost cutting).

As has been the case in recent months, we are maintaining an elevated level of cash to take advantage of short-term opportunities and market volatility which, given the level of unpredictability associated with interest rates, inflation and growth, seems likely to persist in the months ahead.

The events of the past quarter are a helpful reminder that financial markets are full of uncertainties.

Take for example SVB. By early February, it was one of the best performing bank shares of 2023. By mid-March, the shares had been suspended (having fallen 70% from the highs) and the company taken over by regulators.

Whilst we’re not necessarily suggesting there will be ‘another SVB’, the rest of the year will likely be equally challenging.

There are difficult central bank policy dilemmas ahead. The hard versus soft landing debate still rumbles on. And we’re rapidly approaching quarterly earnings season – which will not only inform as to the shape of the downturn and potential recovery, but also provide more data on how the banking sector is coping with the SVB fall out.

What can investors’ do in these uncertain times?

We have favoured a balanced approach.

We’ve been adding risk where opportunities arise. Scaling back when the fundamentals have clearly changed. And ‘biding our time’ in instances where we don’t have a particularly strong view or where the risk-reward is unclear.

Besides raising cash in a number of strategies in anticipation of opportunities ahead, where opportunities have presented themselves recently, we’ve used the market volatility to add to existing holdings at more attractive prices, and find good entry points for new positions – particularly within healthcare and utilities. Elsewhere, we’ve been rotating our exposure among IT names. We’ve also not been afraid to cut our losses when warranted. Some of the US regional banks are an example of the latter. Even though shares across the sector have fallen dramatically, the likely cost of increased regulation and oversight will mean structurally lower profitability and returns.

But we also remain nimble.

Even as long-term investors it’s important not to become entrenched or dogmatic with one’s views or positions. This is particularly the case in rapidly-changing financial markets.

Facts can change. Share prices and valuations can change even faster.

Be mindful of the challenges ahead. But be prepared to capitalise on the opportunities that these will inevitably create.

Michael Stiasny,

Head of UK Equities

Remain alert to potential value opportunities

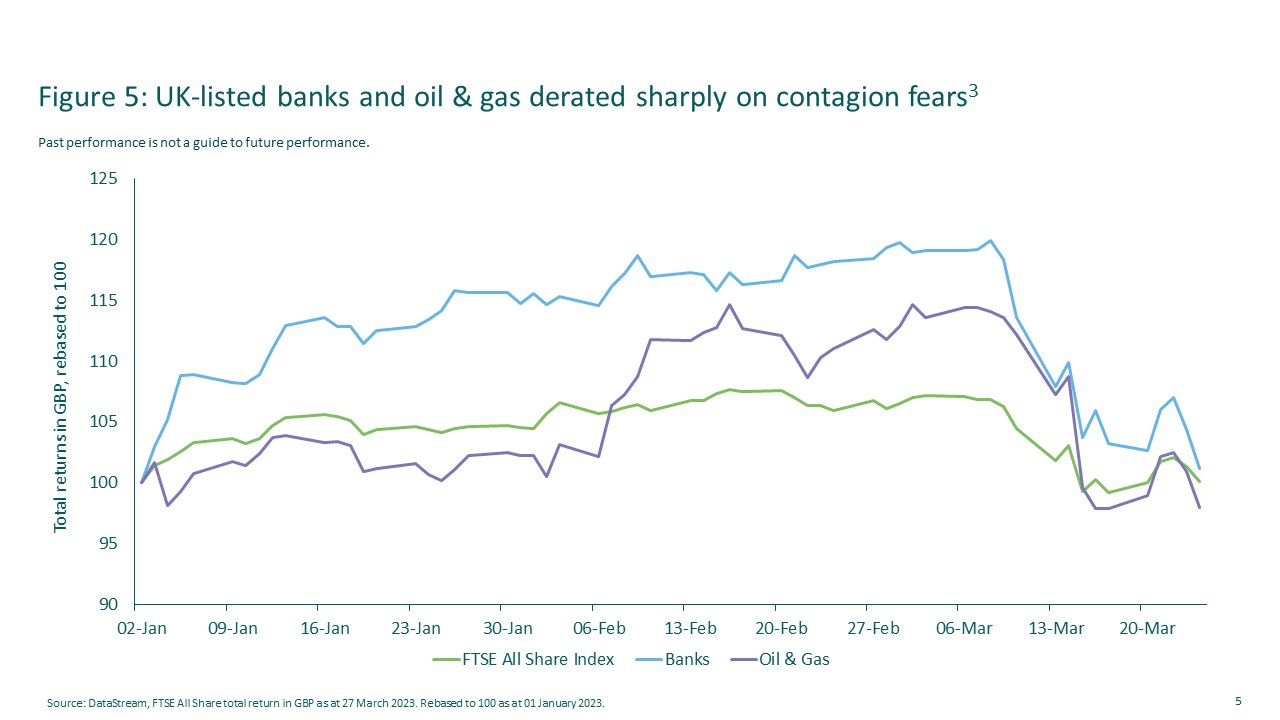

The first two months of 2023 saw a continuation of many of the themes that drove the market in the latter part of 2022. Domestic stocks steadily recovered from the Truss mini-budget; earnings momentum continued to positively surprise as global economies were more resilient than feared; and the FTSE 100 Index continued to keep pace with the mid-caps, as oil & gas and banks in particular led the market returns.

This narrative came to abrupt halt in mid-March, as fears of financial contagion grew following the collapse of SVB and agreed takeover of Credit Suisse by UBS. Despite these banks’ relatively unique circumstances, the impact on the FTSE All Share Index was severe, giving up its 6.9% year-to-date gains to 8 March 2023 to finish the quarter up 3.1%2. As Figure 5 shows, the turmoil had a significant impact on oil & gas names and banks, with these sectors reversing nearly all their year-to-date gains in the latter part of the month.

Looking forward, numerous questions arise from the recent turmoil: is the financial system sound? What is the right cost of equity for a bank? What will be the impact on the real economy if credit conditions tighten? Have interest rates peaked? Will sector/style leadership change?

All these questions have potentially profound implications for markets. Perhaps the simplest way to position a portfolio is to focus on fundamentals and ensure valuations are underpinned by robust balance sheets, good yield support and dividend cover. Following the recent sell off, the FTSE All Share Index is well capitalised, with a net debt-to-EBITDA* ratio of just 1.3x, and now trades on a 12-month forward price-to-earnings (P/E) ratio of 10.1x. Meanwhile, the 12-month forward dividend yield is 4.5%, implying dividends are more than twice covered by prospective earnings4.

2 Source: Datastream, FTSE All Share total return in GBP as at 8 March 2023 and 31 March 2023.

3 Source: Datastream, FTSE All Share total return in GBP as at 27 March 2023. Rebased to 100 as at 01 January 2023.

4 Source: Factset 28 March 2023.

* EBITDA = Earnings before interest, taxes, depreciation and amortisation.

Maintaining a diverse range of holdings will also be important. Confidence has rapidly collapsed and, whilst it is tempting to solely hide in defensive names, a trigger for confidence to reassert itself could emerge and quickly result in a rotation back to more cyclical sectors.

From a bottom-up perspective, the questions around market leadership are particularly relevant. If interest rates have peaked and market leadership moves away from ‘value’ sectors, which other areas of the market could come to the fore? Obvious immediate beneficiaries would be consumer staples and pharmaceuticals with their ‘long duration’, defensive earnings. However, we also believe it is worth looking at other underperforming sectors, which may also benefit from a revised outlook for interest rates, even if their earnings remain somewhat cyclical. This would include the UK housing stocks – which now trade at around book value, with clear signs of incrementally improved trading – and UK real estate (which includes REITs) – trading on a 26% discount to forward net asset value (NAV)5, even though much of the adjustment to cap rates may have already taken place.

In summary, the events of March have reminded us how quickly markets can change when unexpected things happen. Hence, in looking ahead to the second quarter, all we can really say with any confidence is that we expect markets to remain volatile, and we remain alert to exploit potential value opportunities when they occur.

5 Source: Panmure Gordon research, 27 March 2023.

Carl Vine,

Co‐Head of Asia Pacific Equities

Big picture stars aligning?

We continue to be optimistic about the structural outlook for stock-market earnings growth in Japan. This optimism is based on the dynamic of ongoing self-help as the corporate sector continues to take advantage of low-hanging fruit to increase margins and optimise both corporate structures and strategies. We like this self-help story because it doesn’t require a strong macro tailwind.

However, it is worth noting that there may indeed be an emerging macro tailwind that adds some spice to the story. The dynamic for domestic wages in Japan in now changing meaningfully. It is not implausible that the domestic economy starts to experience some self-sustaining growth in the years ahead, as consumption responds to higher wages. This does not seem to be on the radar screen for most investors.

Finally, some pay increases

Japan’s unions recently secured significant increases in this year’s shunto pay-bargaining round; the mean increase appears to be in the region of 4%, above market expectations. Labour shortages are driving up wages in many sectors of the economy across skilled, unskilled, part- and full-time workers alike. The unemployment rate looks set to return towards levels last seen in the early 1990s (ca. 2%), while new job openings continue to climb back toward pre-COVID highs. Ongoing wage rises of 3-5% in the coming few years seem increasingly likely. Compared to cash earnings growth in the prior two decades of almost zero, this represents a significant change. Two key questions leap out; will this lead to higher consumption, and will corporate profit margins suffer?

On the consumption front, whilst the 4% wage round is roughly equal to current headline rate inflation, easing energy prices and a slightly stronger yen suggest the Consumer Price index (CPI) trends towards 2% over the balance of 2023. Combined with ongoing re-opening normalisation, it is easy to imagine this helpful rise in real incomes drives domestic demand growth above current expectations.

In terms of profit margins, other things equal, higher wages should squeeze margins. However, this assumes productivity doesn’t change when, in fact, we see significant ongoing gains in corporate productivity, certainly in the listed corporate sector. Moreover, it assumes that product prices are not being increased to offset rising input costs, which is also happening.

In general, while economies elsewhere are trying to contain wage-price spiral dynamics, Japan is encouraging them. Higher real wages, higher productivity, higher real growth, modestly positive inflation and higher nominal growth can easily take place with flat if not rising margins.

A positive feedback loop between prices and wages is entirely plausible in Japan, which would add a meaningful potential tailwind to what we believe is already a compelling outlook for stockmarket profits growth.

Dave Perrett,

Co‐Head of Asia Pacific Equities

Preparation allows us to look through the noise

After what was a tumultuous 2022, there has been little respite from the various cross currents that have buffeted markets during the first quarter of 2023. While supply disruption eased around the globe and China emerged from the zero-COVID policy, these concerns have been replaced by global banking fears, particularly in Western markets – creating considerable volatility in Asian financial stocks and short-dated interest rates. More specific to Asia, Sino-US tensions, after a brief cooling at the end of 2022, have ratcheted higher again with renewed US technology sanctions and Xi Ji Ping’s visit to Russia.

While there is a lot of ‘news’ in the world at present, we remain focused as a team on bottom up, differentiated research. Indeed, rather than aspire to answer big macro questions, our focus is to continually engage with portfolio and research universe companies to understand the key mediumterm drivers of their business and if these important trends are sustaining or changing. The end result of our ongoing analysis is not an ability to forecast the near-term outcome better than others, but rather to establish some broad sense of what the medium-term underlying valuation of a company should be. This preparation allows us to look through the ‘noise’ surrounding periods of market disruption and use excessive stock price volatility or misplaced contagion fears to our clients’ advantage.

For example, we added to our core China holdings early in the fourth quarter of 2022, when sentiment was especially poor around all things China. More recently, we have reduced exposure to perceived China re-opening ‘winners’, which had rallied aggressively, and allocated resources to long-term structural growth areas that fell out of favour, like certain renewable energy companies. Potential future opportunities include regional financials, should they get caught up in further global contagion fears, with a number of banks we hold being better capitalised and running more conservative balance sheets than their global peers. In addition, these banks also run much more ‘plain vanilla’ banking operations. There are also a number of cyclical companies that we follow, which could be temporarily vulnerable to global growth fears. While we are not in a position to forecast global demand any better than the market, we do have the ability to identify industries where supply conditions are very tight compared to historical standards.

In summary, we are continually striving to position our research effort and portfolio construction in a manner that allows us to take advantage of market disruption rather than having to forcibly react to it.

Michael Bourke,

Head of Emerging Market Equities

Prediction is folly in EM, preparedness comes through experience

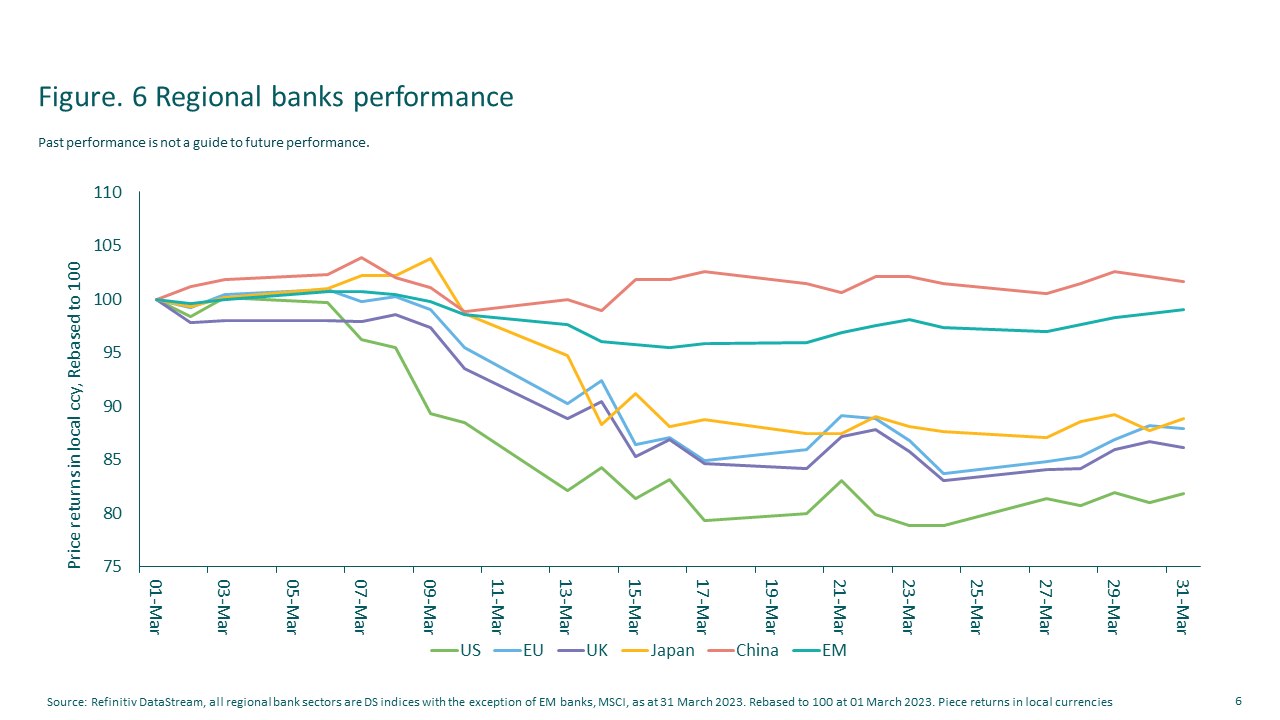

Markets in the first quarter of 2023 were driven by a bout of bank-induced mania with much time being spent pondering the demise of SVB and Credit Suisse. It was fascinating to see the resilience shown by Emerging Market (EM) banks and, in particular, Chinese banks which have performed very defensively:

Across EM banks, Available For Sale (AFS) assets are marked to market and gains/losses taken to capital. EM financials have also not been exposed to the long bond market rally ahead of the recent tightening in US dollar rates – local EMs have never cut rates to the same extent. There is much lower risk of skeletons in the closet. Within insurance, in the chase for yield, western companies have added many more BBB-rated corporate bonds which are vulnerable to downturn in a recession scenario, not to mention more vulnerable to rising rates or a buyer’s strike. Again, EM insurers have not engaged in the same activity. For these reasons, we maintain an overweight in financials across EM and do not see the channels of contagion from recent events.

Where EM financials could be impacted is via the risk of a protracted slowdown/hard landing scenario in the US and Europe which would slow growth in EM, and inevitably pose the normal risk for banks of asset quality issues being higher than expected. A risk we are mindful of and monitoring. That said, we think there is decent margin of safety in the sector overall as it trades at a significant discount to other sectors within EM, for potentially higher returns. Knowing our holdings intimately and being prepared to evaluate new opportunities using our well-defined process have allowed us to navigate this bout of pain successfully and sow new ideas.

The Fed reaction here could act as a catalyst for EM markets to find more solid footing. If the Fed pauses rate hikes, that would give EM central banks breathing space to cut rates from elevated levels. Once the current risk-aversion episode ebbs, the US dollar may weaken, which would also provide a favourable backdrop for EM equities.

The bottom line, we continue to see positive catalysts for EM given the starting point of attractive valuations and improving margin scenario for corporates. China re-opening helps underpin that confidence, even though long-term challenges faced by investors in China persist.

John William Olsen,

Head of Impact Equities

Build in resilience to deal with external shocks

It was an interesting first quarter in 2023! The ripple effects of rapid monetary tightening are revealing cracks in the financial system, which in hindsight seemed obvious – but they were not. Our outlook last quarter did not mention regional bank runs in the US or Swiss investment bank troubles as possible market surprises this year. It was an interesting first quarter in 2023! The ripple effects of rapid monetary tightening are revealing cracks in the financial system, which in hindsight seemed obvious – but they were not. Our outlook last quarter did not mention regional bank runs in the US or Swiss investment bank troubles as possible market surprises this year. The banking system is built on trust and leverage, making it very fragile when confidence is lost, and it is societally expensive to fix when broken. Credit Suisse had, arguably, been struggling for a while, but the developments at otherwise healthy banks caught most by surprise and kept investment professionals glued to their screens.

There was a specific sustainability angle to the downfall of SVB. The bank was widely held by sustainability-oriented funds, because it didn’t finance the fossil fuel industry and had a chunk of its loan book in renewable energy technology companies.

This further fuelled the politically loaded ‘in favour of versus against ESG’ discussion in the US, and even led a prominent governor to blame the failure directly on the bank’s Diversity & Inclusion initiatives. The company did have good social policies in place, matching their California-dominated stakeholder base, but we believe that most would agree that the causality argument is flimsy.

We are all busy thinking about where the next crack might appear, and what the ripple effects might be, but situations like this highlight the importance of the (sometimes less obvious) responsibilities of a portfolio manager. Not predictions, but portfolio risk management skills and single-company due diligence rigour. Both are especially important at times of elevated liquidity risk – and liquidity risk is clearly elevated as the era of easy money comes to an end.

Resilience of business models and robustness of balance sheets will be key requirements if liquidity becomes harder to access. In our strategies, we perform vital assessments of companies’ quality, staying power, financial strength and general ability to deal with external shocks. Our Impact strategies are mandated to also invest in younger, pioneering companies with strong growth potential. This makes the resilience assessment even more vital, because small and growing companies are more vulnerable if access to capital becomes scarce and more expensive. However, these companies form only a small part of each strategy, and they typically have a flexible cost base, low capital requirements and strong balance sheets. The risk from these companies is also balanced with those generating plenty of cash and good, steady returns. We have not identified the need to make any material strategy changes in preparation of potential future cracks. At the margin, we have trimmed some strong performers, and added selectively to some IT holdings at what believe will prove to be very attractive entry points. In line with our thoughts from last quarter, we would not rule out more ‘unexpected’ surprises ahead.

Ed Booth,

Deputy Head of Equity Research and Global Banks Analyst

Turning up the heat on banking stocks

Markets have been shocked by the speed of the deposit withdrawals at certain banks in the age of 24/7 mobile banking (with ca. 25% of deposits taking flight at two institutions within a day).

Meanwhile, higher interest rates are impacting those US regional banks that loaded up on longer duration securities to protect their earnings power when interest rates were at all-time lows. They now face the deepest inversion of the yield curve (in size and duration) since the early 1980s, alongside persistent deposit outflows due to quantitative tightening and due to clients searching for higher interest rates on their savings. These are particular challenges for banks, whose very social purpose is to transform customers’ overnight deposits into long-term lending into the economy.

The market has concerns about Commercial Real Estate and imbalances created by shadow banks for similar reasons. In short, these circumstances replace a similarly unique market consensus of ‘lower forever’ just two years ago, which left several parties holding long-duration assets at low yields that are funded by short-duration liabilities. These are now rising rapidly in cost. Banks, like markets, failed to predict the range of potential outcomes during the depths of the pandemic.

What next? There will likely be some further stresses from the factors above that impact the most exposed monoline business models in particular. Regulators will also respond to each of the issues above, tightening conditions for those banks that are most exposed. This is especially true for previously more lightly-regulated US regional banks.

It will likely also force assumptions on all banks that deposit outflows will be faster when a bank is stressed, reflecting the new realities of Twitter and mobile banking.

Against this backdrop, there are some relative winners within banks.

The largest banks in the US (and most banks in Europe) are more resilient to these issues. Interest rate exposures and deposit stickiness are already stressed routinely (via a range of oversight measures, such as Liquidity Coverage Ratios, Net Stable Funding Ratios, Interest Rate Risk in the Banking Book) and these banks’ Available For Sale (AFS) portfolio losses are marked to market every quarter. This has kept interest risk lower at those banks and has also pushed them to diversify their earnings. These are diversified, ‘universal’ banks, which cater to a diversified set of customers, and derive profits from different parts of the yield curve and from non-banking businesses. They are away from the eye of the storm.

Equally, while deposits are starting to show movement from current accounts to higher yielding time deposits in the Eurozone, bank regulations are already tighter with respect to liquidity, the yield curve is less inverted, and interest rates have risen less sharply. The latter two factors mitigate both deposit flows and asset risks – the two issues that are front and centre today. If economic and interest rate pressures are able to ease soon, and current market worries abate, these banks will also be in position to earn materially-better returns in the next cycle than they did in the last, which would support long-term valuations.

The extreme change in developed market interest rates illustrates again that preparation, via diversification and sensible regulation, helps manage pain. There will, undoubtedly, be some more pain from such a rapid return to interest rates not seen in developed markets for 15 years.

But the strongest banks will outperform those fears. We already see some valuation opportunities among them, assuming that a material recession is avoided.

Leonard Vinville,

Head of Convertibles

Being selective is key to delivering better risk-adjusted returns

As convertible investors, we can deal with the uncertainties ahead by playing on three main levers: credit quality, option technicals or structure, and equity.

Credit offers us a rich vein of investment opportunities. We think that in the US and Europe, credit spreads have normalised into our fair 400-500 basis points (bps) range for crossover names. These spreads, coupled with higher interest rates, provide attractive yields. In Asia, high yield (HY) credit spreads have widened substantially during this past quarter, providing cheap valuations. To top it up, we find that convertible implied spreads are often wider (cheaper) than pari passu (equivalent) straight bonds, both for ‘at-the-money’ and for ‘busted’ convertibles1.

For equities, though, we are less confident on their valuations given the macroeconomic and earnings risks ahead. US equities are still richly valued while European and Asian valuations are cheaper overall (even after considering sector and growth differentials), but we remain more constructive on spreads (credit valuations) than on equities in the current environment.

The events in the banking sector in March are a reminder of the need to be prepared for what we do not know is coming. For us, that means being highly discerning when choosing our investments. Our game plan involves buying the right convertible structure, not just the right stock name. We look for at-the-money, convex convertibles with good credit quality, low distance to the bond floor and enough delta# to remain exposed to equity upside should the underlying stocks go up in price, but which fall by a lesser degree if the underlying stocks go down. We also focus on companies with better business models and proven free cashflow (FCF) generation capabilities. An example of this is our investment in a convertible issued by a cancer radiology diagnostic provider. This is a BB shadow-rated business, its established activities provided a good bond floor, and the stock was trading at a discount to its fair value. In addition, its clinical pipeline was not priced in by the market, providing further valuation support, while the at-the-money option embedded in the convertible allowed us to participate in the equity upside.

Although new issuance volume year-to-date is running in line with our expectations, with an increased variety of issuers and attractive terms and conditions versus the past couple of years, given our high degree of selectivity, we have only participated in around 13% of new issues this year.

We have a broad universe from which to identify investment opportunities. We look across the entire investment universe (both existing and new issues) when seeking investments with attractive risk-reward properties but, as ever, we remain selective in our approach. We also create opportunities by maintaining flexibility in the way invest. For instance, with a travel and tourism investment, we combined a low-delta convertible with high implied spread for an investmentgrade issuer with a stock position, to benefit from the recovery in travel and tourism. For a Chinese property developer, we invested in two different straight bonds and the stock itself, as we believed the synthetic exchangeable bond was too short-dated and had insufficient delta. For a French hotel chain investment, we chose to invest in its perpetual bond at a high yield rather than its convertible, as we felt the equity valuation was not cheap enough. In Asia, we have invested in a convertible issued by a Chinese food delivery, travel and eCommerce provider. This convertible has relatively low delta but is trading at an implied spread wider than its investment-grade bonds, despite being two years shorter in maturity, and offers an equity option virtually for free.

Selection is critical. Through thorough analysis of the option characteristics and by maintaining a flexible investment approach – comparing opportunities across companies’ corporate structures, instruments (convertibles, straight bonds, stocks) and credit segments (non-rated, investment grade and high yield) – we can choose the convertible structure that we believe offers the best risk-reward opportunity and can deliver better risk-adjusted returns for our clients.

1 ‘At the money’: when an option’s strike price is the same as the current market price of the underlying security; ‘Busted Convertible’: a convertible bond where the underlying stock trades far below its conversion price.

# Delta compares the change in price of an option with that of the underlying security. It can help portfolio managers determine how option prices are likely to rise or fall as the underlying security price varies.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.