Equities

Exploring the ‘III’ framework and methodology

10 min read 21 Jun 23

III framework

The III framework – Investment, Intention, Impact – is a practical means of evaluating candidate companies for M&G’s public equity impact funds. The framework is designed to robustly and consistently apply set criteria and standards for rating the impact and investment case of these companies. Only companies that score an above-average rating (i.e. above 5/10 for each pillar) are included in our watchlist. This list consists of impactful, quality companies that we can buy when the timing and price are right.

The score for each ‘I’ pillar is derived from the assessment and rating of its key drivers, fully outlined in this document. We aim to achieve an optimal balance of quality companies, with a clear purpose consistent with management’s vision and strategy. We believe that this will enable a company to effectively create positive environmental, social and/or economic impact for the regions and people it serves.

‘Double compounding’

Only companies with quality business models, capable of growing sustainably over the long term, will pass the III framework. While this is important for the funds’ objective of generating attractive financial returns, it also allows us to benefit from the concept of ‘double compounding’. In other words, the compounding of both investment returns and positive societal impact over time. Given the fundamental alignment between the company’s core business and the positive impact it generates, the company can reinvest the returns it generates directly into activities that generate further positive impact.

III score methodology

The overall III impact score is derived in the following manner:

1 Each of the criteria within an ‘I’ pillar is assigned a score from 0-5

2 We then generate a total score for the ‘I’ pillar by summing up the (0-5) scores and generating a percentage, which is represented as a score out of 10.

3 The final III score is the average of each pillar (Investment, Intention, Impact).

Figure 1: III framework

Investment score (out of 10)

There are five broad areas we explore when considering a company’s investment score:

Quality of the business model (out of 5)

We ascertain the strength of the business model, by assessing elements such as: the sustainability of the business model; health of the industry in which it operates; the avenues to growth (organic and inorganic); and the company’s ‘moat’ (i.e. competitive advantages). Performance track record is also key in proving the business case. This helps us establish whether the company is built for longevity and growth and how sustainable its moat is. Ultimately, we aim to invest in strong business models operating in disciplined industries.

Competitive positioning (out of 5)

We are generally interested in companies that have a strong competitive position (i.e., in the top five in terms of market share) in the business areas in which they operate, or have scope to grow this. Points of strong differentiation (e.g. customer relationships, distribution channels, economies of scale, brand strength) versus peers are also key. We tend to favour disciplined companies with strong positions in industries with high barriers to entry.

Capital allocation (out of 5)

Here, we consider the management’s track record on capital allocation by assessing M&A appetite and execution; the overall strength of the company balance sheet (growth and leverage balance); dividend policy and cash and capital management.

Business risk (out of 5)

We aim to consider business and industry-specific risks that the company might face. This also challenges the strength of the moat, the business model and possible risks to it. Ultimately, we want to understand how material the effect of internal and external risks could be to the sustainability of the business model over a period of 10 years.

ESG risk (out of 5)

We consider a range of material environmental, social and governance issues that represent potential risks to the long-term sustainability of a company. This is separate to a company’s impact case, and includes areas like board composition, climate target setting and employee satisfaction.

Liquidity (out of 5)

The liquidity profile of the company is essential when establishing the investability of the candidate stock. We aim to create a balanced portfolio of impactful companies across the market cap spectrum, with liquidity management being an important aspect of portfolio risk management. The portfolio diversification across ‘Pioneers’, ‘Enablers’ and ‘Leaders’ supports this diversification across both earlier-stage businesses and those with a more mature, usually more liquid, profile.

Intention score (out of 10)

There are three broad areas we explore when considering a company’s Intention score:

Mission statement and purpose (out of 5)

The group’s mission statement, vision or purpose should generally reflect the impact case. This indicates that the company’s purpose is heavily aligned to driving impact, giving us confidence that management is likely to operate with this in mind over the long term.

However, there are several cases in which a company’s mission or vision may not overtly mention the positive impact case, but the business model is heavily aligned to positive impact. ‘Enablers’ (companies which help the end-customer achieve positive impact), tend to fall into this category. Given this, the alignment of the business model is key in giving some credit to companies whose mission statement might fall short of including the impact case, but whose daily activities and business strategy generates significant positive impact anyway.

We also assess companies whose mission statements may have impact-related statements, but whose business model or strategy may not entirely fulfil this mandate. In such a case, a call is made on whether the intentions of the company are genuine and consistent with the business’ strategy/vision.

Strategic alignment and culture (out of 5)

We probe the track record of the management team, by assessing business performance under its leadership, consistency of the strategy and general market and our perceptions of the management team. We also consider the composition and track record of the board, focusing on the independence (are Chairman and CEO roles combined, for example), the tenure (is it an entrenched board) and the female representation on the board. We have used employer-review website Glassdoor to get a sense of the culture of the firm as well, to gauge its consistency between management strategy and the experience of employees.

Implementation (out of 5)

Execution on the group’s impact case and business alignment to this is another measure we use to ascertain the candidate company’s intentionality. This may include the plans set forth to reach impact targets and the progress or impact already created by the business model. This helps us understand whether the company has fully committed to driving positive change.

Impact score (out of 10)

There are five areas we explore when considering a company’s impact score:

Primary impact (out of 5)

The primary United Nations Sustainable Development Goal (SDG) and key performance indicators (KPIs) the candidate company is addressing – the SDG on which it has the most material impact.

Net impact (out of 5)

The primary SDG and KPI it is addressing, as well as other secondary SDGs and KPIs it is addressing.

We also investigate any negative impacts the company may have. This should either be non-existent or immaterial to overall group revenues or profitability (less than 10%).

Measurability of the impact (out of 5)

This looks at the ability to measure the impact generated by the company (i.e., carbon emissions avoided or number of patients treated). This generally represents the number of people impacted by a company’s activities or how far-reaching the impact is.

This may be more difficult to get from ‘enablers’, as their contribution to the positive impact case is likely more indirect since it depends primarily on the end market user. In general, published disclosure may not fully give us a sense of this. Therefore, dialogue with management tends to provide greater colour on the impact generated.

Materiality of impact (out of 5)

This represents revenues that relate to sustainability or social activities (i.e., revenues to SDGs). We believe that if the revenues stemming from SDG-related activities are material in the context of the group operations, this will likely be a major driver of the strategy and represent sustainability of the positive impact created.

Additionality (out of 5)

We consider the question of how the world/region would look if the candidate company did not exist. Here we consider elements such as the scale of the company (market share) and reach (number of regional and global offices), and valuable aspects of the business model that are difficult to replicate (e.g., the strength and scale of the distribution network).

Impact risk (out of 5)

We evaluate the likelihood that the company’s impact will be different than expected. We will consider factors such as the quality of the available impact measurement data, the probability of external factors affecting the company’s impact, the risk of the impact not being executed as expected, and the likelihood of an unexpected positive or negative impact occurring.

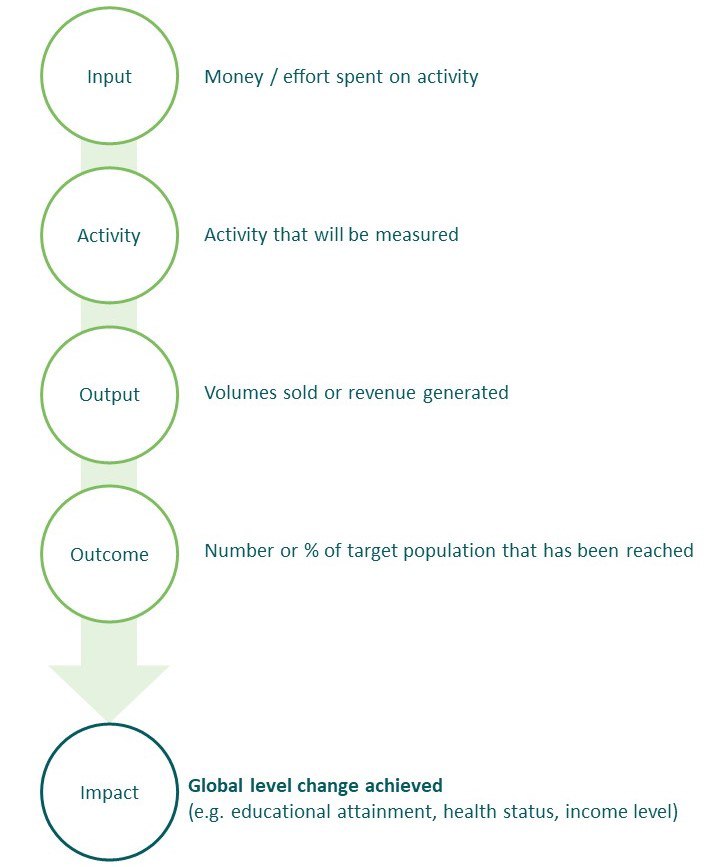

Results chain

As part of our efforts to evaluate the impact and direct our focus on the variables that are within a company’s control, we have adapted the ‘results chain’ framework used by impact-oriented organisations and agencies such as the World Health Organisation and the Gates Foundation. This helps map the route to (or the logic of) impact from start to finish.

Figure 2: Results chain

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.