Equities

M&G (Lux) Global Listed Infrastructure Fund - Attractive opportunities to harness structural trends

7 min read 25 Sep 23

Outlook

- Perceived interest-rate sensitivity has acted as a drag on listed infrastructure as an asset class. But for us, fear creates opportunity, and we strongly believe that today's valuation level presents a highly attractive entry point for long-term investors.

- We remain resolutely optimistic about the long-term prospects for listed infrastructure, as we believe that powerful structural trends continue to drive growth in the asset class. The energy transition remains a key theme in the fund; we also believe artificial intelligence (AI) has the potential to enhance long-run growth in infrastructure.

- We continue to see inflation-beating dividend growth from the majority of the fund's holdings, and have been active in replacing companies exhibiting low dividend growth with new ideas delivering higher growth. With more potential investment candidates in the pipeline, we remain optimistic about the long-term prospects for the fund.

The value and income from the fund's assets will go down as well as up. This will cause the value of your investment to fall as well as rise. There is no guarantee that the fund will achieve its objective and you may get back less than you originally invested. Past performance is not a guide to future performance. The views expressed in this document should not be taken as a recommendation, advice or forecast.

The energy transition

The energy transition is a theme that features prominently in the fund, with our positive view endorsed by government policies and incentives aimed at addressing climate change. The Inflation Reduction Act (IRA) in the US, for example, has only been in effect for 12 months: the largest-ever investment in clean energy and climate action has only just begun.

Since the IRA became law in August 2022, the US private sector has committed more than US$110 billion in new clean energy manufacturing investments, including more than US$70 billion in the electric vehicle (EV) supply chain and more than US$10 billion in solar manufacturing. US electricity generation from wind is expected to triple and solar generation to increase by as much as eight-fold by 2030 as the world’s leading economy aims to meet its climate goals, build a clean energy economy and strengthen energy security[1].

We believe the ambitious programme is topical and timely. The increasing incidence of extreme weather events and the havoc they bring to communities around the world provide a constant reminder that the task is urgent. The devastating wildfires in Hawaii remain etched in our memories, but provide just one example in a long list of many.

Infrastructure is widely acknowledged as central to the long-term solution, with utilities playing a pivotal role in the development of renewables, the reconfiguration of grids to accommodate new sources of energy, and the development of low-voltage networks fit for the modern age. We believe the tailwind for infrastructure is here to stay.

Infr-AI-structure

Artificial Intelligence (AI) has been the dominant theme in equity markets this year, but NVIDIA is not the only beneficiary of the enthusiasm for this burgeoning technology. AI can help infrastructure businesses to reach new levels of efficiency and ultimately enhance long-term growth in the asset class.

Listed infrastructure provides exposure to the explosive growth in AI by way of data centres, which are critical to AI’s success given the ongoing demand for computational resources. The demand profile bodes well, in our view, for revenue growth and pricing power at data centre companies such as Equinix, which remains a core holding in the portfolio.

AI also has the potential to revolutionise the asset class in other ways. It can facilitate the development of smart grids, which will help optimise electricity distribution and consumption. AI can analyse large amounts of data, including weather, consumption patterns and the status of the network, to help utilities predict energy demand and manage energy resources efficiently. Italy’s Enel, a top 10 holding in the fund, established a subsidiary in 2021, which is dedicated to the provision of smart grid solutions to distribution system operators.

AI can play a crucial role in optimising water resource management. By utilising machine-learning algorithms and real-time data analysis, smart water systems can detect leaks, predict water demand, and optimise water distribution. American Water Works, a core holding in the fund since launch, has been using machine learning to monitor its ageing network of water pipes, detect deteriorating tank coating, and predict water leakage.

Transportation infrastructure companies can leverage AI to improve mobility efficiency and safety. Traffic management systems using AI for predictive analytics can optimise traffic flow, reduce congestion, and enhance road safety. Toll road operators can utilise data analytics to predict demand patterns and dynamically adjust tolls to maximise revenue. Ferrovial, the Spanish toll road company, is developing the Aivia orchestrated connected corridors, a project that uses AI to integrate connected autonomous vehicles safely into our future roads.

We are merely scratching the surface. By incorporating AI, infrastructure is potentially embarking on a new era in which the qualities of its critical assets become even more appealing.

Figure 1: Utilities and real estate, cheapest since COVID times

Past performance is not a guide to future performance.

Source: Refinitiv Datastream, 24 August 2023

Cheapest since COVID times

Perceived interest-rate sensitivity has acted as a drag on listed infrastructure as an asset class, with utilities and companies structured as real estate investment trusts (REITs) bearing the brunt of negative sentiment. The underperformance of US utilities this year, for example, has been the most extreme since the technology bubble in 1999 (Source: Wolfe Research, 4 September 2023).

But for us, fear creates opportunity, and we strongly believe that today’s valuation levels present a highly attractive entry point for long-term investors. The MSCI ACWI Utilities Index and the MSCI ACWI Real Estate Index are trading at their cheapest levels since the global pandemic (see Figure 1), after which time both sectors saw their valuations recover significantly.

This valuation support gives us confidence that the asset class can recover from its recent bout of volatility. We have experienced similar periods of market nervousness in the past. On each occasion, we have acted with conviction by buying into weakness where we think the long-term growth opportunity remains intact, and were subsequently rewarded with bursts of strong performance. We expect the current circumstances to be no different.

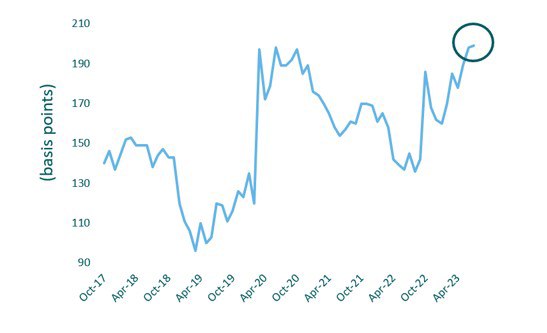

The value we see in listed infrastructure is also manifested in the fund’s yield. The fund’s forecast dividend yield (gross of fees), which stands at 4.1% (as at end of July), offers the highest premium relative to the MSCI ACWI Net Return Index since the fund launched in 2017 (see Figure 2).

The current level of yield is compelling, in our view, for an income stream which we seek to grow in excess of G7 inflation over the long run.

Figure 2: Forecast dividend yield (gross) spread relative to MSCI ACWI Net Return Index.

Forecast dividend yield is an estimate of future performance based on evidence from the past on how the value of this investment varies, and/or current market conditions and are not an exact indicator. What you will get will vary depending on how the market performs and how long you keep the investment/product.

Source: M&G, August 2023

New ideas to accelerate dividend growth

We continue to see inflation-beating growth across the portfolio, with the majority of holdings increasing their dividends in the core 5-10% range. But we are not resting on our laurels. We have been active in replacing companies exhibiting low dividend growth with new ideas delivering higher growth – high enough to potentially offset the ravages of persistent inflation.

We divested CCR, the Brazilian toll road operator, owing to concerns about the lack of dividend growth, and we have earmarked others for the same treatment on the same grounds.

We are also delighted with the quality of investment opportunities available in the current market environment. The recent purchases of Kamigumi (Japan’s largest port operator) and Getlink (French operator of the Channel Tunnel infrastructure) provide good examples. Both companies are not only proud owners of unique critical infrastructure, but they also boast strong shareholder value credentials by way of impressive dividend growth. Both stocks offer long-term attractions without having to overpay for the privilege, in our view.

Being selective will be paramount in these volatile times. With more potential investment candidates in the pipeline, we remain optimistic about the long-term prospects for the fund.

Fund description

The fund aims to deliver a combination of capital growth and income that is higher than that of the global equities market over any five-year period while applying the fund’s environmental, social and governance (ESG) criteria and sustainability criteria and to increase the income stream every year, in US dollar terms. It looks to do this by investing at least 80% of the fund in shares issued by infrastructure companies, investment trusts and real estate investment trusts of any size, from any country, including emerging markets. The fund usually holds shares in fewer than 50 companies. Infrastructure companies include businesses in the following sectors: utilities, energy, transport, health, education, security, communications, and transactions. ESG and sustainability considerations are integrated into the investment process.

The main risks associated with this fund:

- The fund can be exposed to different currencies. Movements in currency exchange rates may adversely affect the value of your investment.

- Investing in emerging markets involves a greater risk of loss due to greater political, tax, economic, foreign exchange, liquidity and regulatory risks, among other factors. There may be difficulties in buying, selling, safekeeping or valuing investments in such countries.

- The fund holds a small number of investments, and therefore a fall in the value of a single investment may have a greater impact than if it held a larger number of investments.

- In exceptional circumstances where assets cannot be fairly valued, or have to be sold at a large discount to raise cash, we may temporarily suspend the fund in the best interest of all investors.

- ESG information from third-party data providers may be incomplete, inaccurate or unavailable. There is a risk that the investment manager may incorrectly assess a security or issuer, resulting in the incorrect inclusion or exclusion of a security in the portfolio of the fund.

- The fund could lose money if a counterparty with which it does business becomes unwilling or unable to repay money owed to the fund.

Other important information:

- Please note that the fund invests mainly in company shares and is therefore likely to experience larger price fluctuations than funds that invest in bonds and/or cash.

- Investing in this fund means acquiring units or shares in a fund, and not in a given underlying asset such as a building or shares of a company, as these are only the underlying assets owned by the fund.

- For explanation of technical terms, please refer to the glossary via the link https://docs.mandg.com/docs/glossary-master-en.pdf

Further risk factors that apply to the fund can be found in the fund's Prospectus.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.