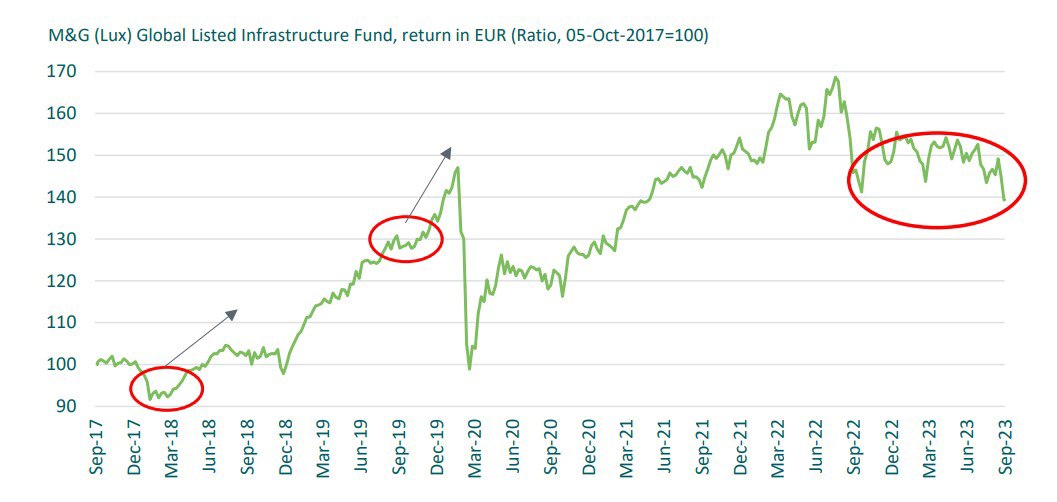

Source: Datastream, 30 September 2023. Rebased to 100 at 5 October 2017. Euro A Acc shares, income reinvested price to price

New ideas seeking to accelerate dividend growth

We continue to see inflation-beating dividend growth across the portfolio, with the majority of holdings increasing their dividends in the core 5-10% range. But we are not resting on our laurels. We have been active in replacing companies exhibiting low dividend growth with new ideas delivering higher growth – high enough to offset the ravages of persistent inflation.

We divested CCR, the Brazilian toll road operator, owing to concerns about the lack of dividend growth, and we have earmarked others for the same treatment on the same grounds.

We are also delighted with the quality of investment opportunities available in the current market environment. The recent purchases of Kamigumi, the Japanese ports company, and Getlink, the owner and operator of Eurotunnel, provide a case in point. Both companies are not only proud owners of unique, critical infrastructure -- they also boast strong shareholder value credentials by way of impressive dividend growth. Both stocks offer long-term attractions without having to overpay for the privilege.

Being selective will be paramount in these volatile times. With more potential investment candidates in the pipeline, we remain optimistic about the long-term prospects for the fund.

Fund description

The fund aims to deliver a combination of capital growth and income that is higher than that of the global equities market over any five-year period while applying the fund’s environmental, social and governance (ESG) criteria and sustainability criteria and to increase the income stream every year, in US dollar terms. It looks to do this by investing at least 80% of the fund in shares issued by infrastructure companies, investment trusts and real estate investment trusts of any size, from any country, including emerging markets.

The fund usually holds shares in fewer than 50 companies. Infrastructure companies include businesses in the following sectors: utilities, energy, transport, health, education, security, communications, and transactions. ESG and sustainability considerations are integrated into the investment process.

Outlook

We strongly believe that the market’s aversion to perceived interest rate sensitivity provides an attractive entry point for a strategy capable of delivering real growth over the long term in excess of G7 inflation by way of growing dividends. The powerful tailwinds driving infrastructure are as robust as ever, in our view.

The energy transition, for example, is a theme that features prominently in the fund, our positive view endorsed by government policies and incentives aimed at addressing climate change. The Inflation Reduction Act (IRA) in the US has only been in effect for 12 months; the largest ever investment in clean energy and climate action has only just begun.

Since the IRA became law in August 2022, the US private sector has committed more than $110 billion in new clean energy manufacturing investments, including more than $70 billion in the electric vehicle (EV) supply chain and more than $10 billion in solar manufacturing. US electricity generation from wind is expected to triple and solar generation to increase as much as eight-fold by 20301 as the world’s leading economy aims to meet its climate goals, build a clean energy economy and strengthen energy security.

The ambitious programme is topical and timely. The increasing incidence of extreme weather events and the havoc they bring to communities around the world provide a constant reminder that the task is urgent. The devastating wildfires in Hawaii remain etched in our memories, but provide just one example in a long list of many.

Infrastructure is widely acknowledged as central to the long-term solution to climate change, with utilities playing a pivotal role in the development of renewable energy sources, the reconfiguration of grids to accommodate new sources of energy, and the development of low-voltage networks fit for the modern age. We believe the tailwind for infrastructure is here to stay.

We remain resolute in our pursuit of long-term growth opportunities, which in our opinion are abundant across the asset class. Six years into our listed infrastructure journey, our conviction has never been stronger.

The main risks associated with this fund:

- The fund can be exposed to different currencies. Movements in currency exchange rates may adversely affect the value of your investment.

- Investing in emerging markets involves a greater risk of loss due to greater political, tax, economic, foreign exchange, liquidity and regulatory risks, among other factors. There may be difficulties in buying, selling, safekeeping or valuing investments in such countries.

- The fund holds a small number of investments, and therefore a fall in the value of a single investment may have a greater impact than if it held a larger number of investments.

- In exceptional circumstances where assets cannot be fairly valued, or have to be sold at a large discount to raise cash, we may temporarily suspend the fund in the best interest of all investors.

- ESG information from third-party data providers may be incomplete, inaccurate or unavailable. There is a risk that the investment manager may incorrectly assess a security or issuer, resulting in the incorrect inclusion or exclusion of a security in the portfolio of the fund.

- The fund could lose money if a counterparty with which it does business becomes unwilling or unable to repay money owed to the fund.

Other important information:

- Please note that the fund invests mainly in company shares and is therefore likely to experience larger price fluctuations than funds that invest in bonds and/or cash.

- Investing in this fund means acquiring units or shares in a fund, and not in a given underlying asset such as a building or shares of a company, as these are only the underlying assets owned by the fund.

- For explanation of technical terms, please refer to the glossary via the link https://docs.mandg.com/docs/glossary�master-en.pdf

Further risk factors that apply to the fund can be found in the fund's Prospectus.