Flexible asset allocation showing its worth

6 min read 18 Jan 23

- The year 2022 revealed the need for highly flexible asset allocation strategies

- The fund’s use of shorting (seeking to benefit from a fall in the price of a security) and tactical trades were crucial to delivering a significant positive return

- We should be wary of placing too much faith that the environment experienced last year is at an end

The value and income from the fund's assets will go down as well as up. This will cause the value of your investment to fall as well as rise and you may get back less than you originally invested. There is no guarantee that the fund will achieve its objective and you may get back less than you originally invested.

A great environment for our approach

The year 2022 was one in which the value of active and flexible asset allocation was writ large for investors.

The flexibility and consistent framework of the ‘episode’ strategy meant that it was well placed to deal with the heightened volatility of asset prices experienced last year. The positions taken by the fund included some of the portfolio’s largest-ever short bond exposures, the first short equity positions in more than a decade and a brief period entirely in cash before tactically moving long of assets in the fourth quarter.

The challenge to passive long-only strategies

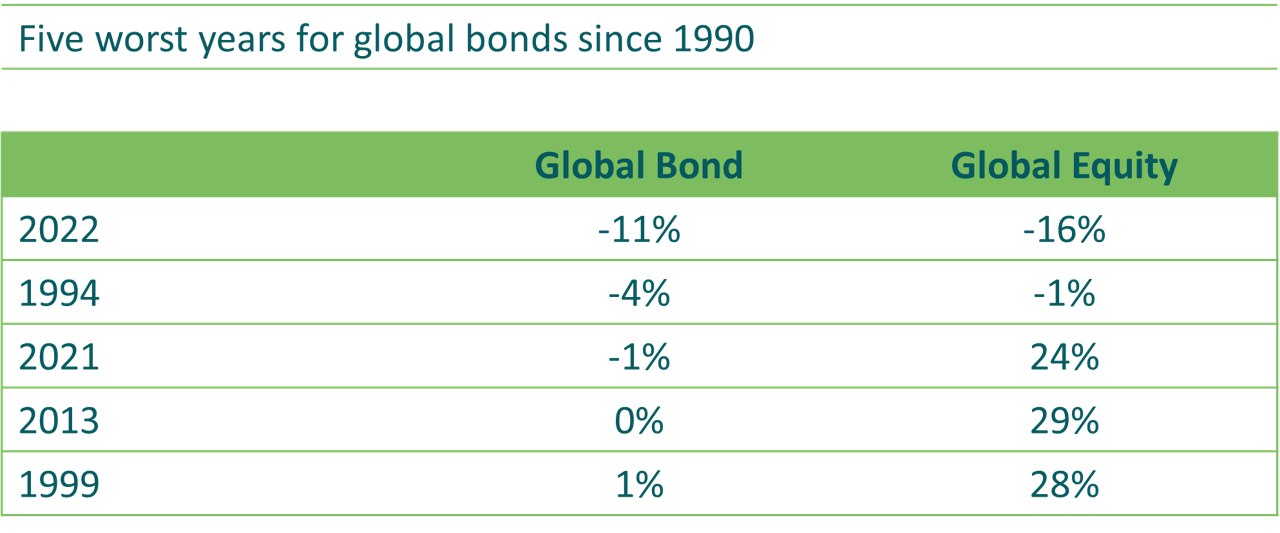

In a break from the experience of many investors’ careers, last year there were double-digit losses from both global equity and global bond markets -- the first time that there have been declines in both the MSCI World and Barclays Aggregate indices since 1994.

Source: Bloomberg, 3 January 2023. “Global Bond” = Bloomberg Global-Aggregate Total Return Index (Hedged), “Global Equity” = MSCI World Net Total Return (local).

Past performance is not a guide to future performance.

As we have discussed in previous notes[1], this was an environment primed for active management to demonstrate its worth. By this we mean strategies that were dynamic, selective and could protect investors from potentially non-recoverable losses.

It was also a set of conditions that were particularly supportive for our ‘episode’ approach, where we aim to take advantage of investors’ emotional and behavioural reactions to events in the markets. Behavioural mispricing was notable and volatility created tactical opportunities, while many traditional investment approaches struggled.

What is an episode?

Episodes are investment opportunities created by the emotional and behavioural biases of investors.

A common episodic dynamic is panic and a focus on the short-term in periods of market stress. Rapid price action and attractive valuations offer opportunities for the strategy to be contrarian.

Episodes can also manifest themselves as complacency or excitement. Investors that are enjoying the ride, or anchored to past experience, can ignore bad news, providing the opportunity to short expensive assets.

How we generated return

The roots of the fund’s returns in 2022 lay in the market conditions that had been created in 2021 -- a year that was frustrating for strategies not prepared to put up with the expensive valuations of many of the better performing assets in that period.

This unwillingness to participate was a shift from much of the period since the financial crisis, in which episodic opportunities had primarily come from ‘buying into panic.’ Even before the pandemic, investors had shaken off much of the fear of volatility and overall negativity. Valuations were no longer obviously attractive, ‘buying the dip’ was widely discussed, and any threats from rising cash rates were dismissed - the ‘Fed put’ was still in play.

In these conditions, the episodic approach suggested that prospective returns were now likely to be driven from a predisposition to take short positions; to us, investors seemed to have become complacent.

Shorting government bonds

The most notable area of complacency at the beginning of 2022 was in developed market government bond yields. At the start of last year, even as core inflation hit 6%, five-year US government bond (Treasury) yields sat below their pre-pandemic levels.

Source: Refinitiv Datastream, Bloomberg, December 2021.

Past performance is not a guide to future performance.

The episode approach does not rely on forecasting what inflation will do next. One merely had to observe that such yields were unattractive in almost any scenario, let along one in which inflation was already elevated.

Over the course of 2021, the fund had moved from long duration exposure at the start of the year, to a duration-neutral curve trade (shorting five-year Treasuries while long 40-year bonds) and finally to outright short duration. In January 2022, this short position (in five-year Treasuries) was increased to 200% of the fund.

Investments in bonds are affected by interest rates, inflation and credit ratings. It is possible that bond issuers will not pay interest or return the capital. All of these events can reduce the value of bonds held by the fund. Investing in emerging markets involves a greater risk of loss as there may be difficulties in buying, selling, safekeeping or valuing investments in such countries.

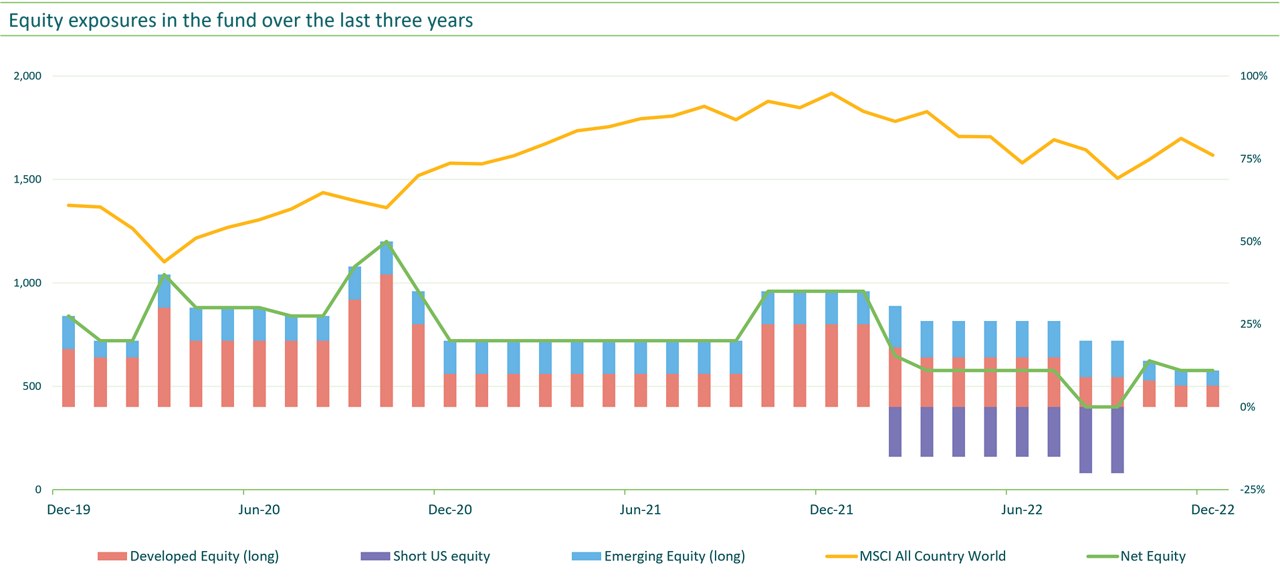

Highly tactical portfolio shifts

While short bond exposure was a key driver of return in 2022, this was not a static position.

Volatility across markets meant that the amount of capital allocated to key portfolio themes varied significantly. For example, we removed the short fixed income position in early May, allowing the portfolio to avoid the bear market rally, before re-establishing it at the end of month. The position was also diversified with the introduction of short positions in German and Italian government bonds at that time.

The fund was also highly dynamic in the equity space. Exposure to the US market was switched from long to short early in the year. Overall equity exposure moved from net long to flat in August and September, before the fund re-engaged with long positions in both bonds and equities at the end of October.

Source: Refinitiv Datastream, M&G, January 2023.

The fund may be highly concentrated at times in a limited number of investments or areas of the market, which could result in large price rises and falls. The fund can be exposed to different currencies. Movements in currency exchange rates may adversely affect the value of your investment.

Investment decisions are made from a top-down perspective, analysing macroeconomic trends, and typically expressed via highly liquid country or sector level derivative instruments (whose value depends on that of an underlying asset such as a stock or bond). This approach has been employed since the late 1990s, being used by a range of investors as a macro strategy in its own right, a portfolio diversifier, as well as an asset allocation ‘overlay’ within portfolios.

The fund may use derivatives to profit from an expected rise or fall in the value of an asset. Should the asset’s value vary in an unexpected way, the fund will incur a loss. The fund’s use of derivatives may be extensive and exceed the value of its assets (leverage). This has the effect of magnifying the size of losses and gains, resulting in greater fluctuations in the value of the fund.

Currency themes

The episode approach to currency management looks to what is known as the ‘carry’ -- the return earned from holding one particular currency, resulting from exchange rate and interest rate differences between that currency and other ones. However, rather than buying a basket of high carry currencies, currency positions are actively managed, looking for episodes of spot rate trauma and assessing the macroenvironmental background.

In 2022 this approach - avoiding short exposure to the US dollar while backing emerging markets - delivered a modest positive return. Funding currencies, such as the euro, Taiwanese dollar and British pound, in which we took short positions, weakened versus those in which we took long exposures. We removed short sterling exposure after sharp falls in September; later, we added long positions in the Polish zloty and Hungarian forint.

What’s next?

Investor complacency on the near-term path for interest rates was well and truly shaken by the fourth quarter of 2022 and, as we enter 2023, the portfolio is more cautiously positioned. We took the tactical opportunity to move long of both Treasuries and equities in October, which resulted in positive returns in the final quarter of 2022. As the episode unwound, we reduced exposure in response.

While there is a lot of negativity about the prospects for growth, there are few signs of capitulation in asset markets. At the same time, there is a strong consensus that inflation has peaked, which has been supportive of asset prices recently. Valuations have improved almost everywhere but, as always, are dependent on the path for cash interest rates and the extent of optimism in profit forecasts.

The current episode approach is, therefore, to be positioned with lots of headroom in our risk budget, to enable us to trade the twists and turns, should either panic or complacency come to dominate market behaviour once again.

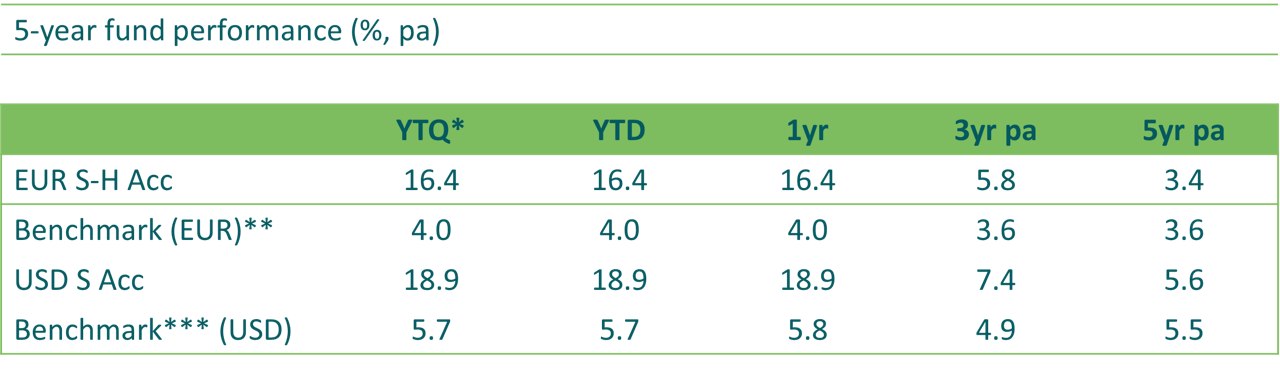

Performance

Past performance is not a guide to future performance.

Source: Morningstar Inc., 31 December 2022. EUR S-H and USD S share classes, income reinvested, price to price.

* YTQ = year to the most recent quarter-end (Q4)

** Benchmark (EUR) = ESTR +4-8%

*** Benchmark (USD) = SOFR + 4-8%

Past performance is not a guide to future performance.

Source: Morningstar Inc., 31 December 2022, EUR S-H and USD S share classes, income reinvested, price to price.

Prior to 3 August 2021 the benchmark for the fund’s EUR-denominated share classes was 3-month EUR LIBOR + 4%. With effect from 3 August 2021 the benchmark is ESTR + 4-8%. For the USD-denominated share classes, the benchmark was 3-month USD LIBOR + 4%; it is now SOFR + 4-8%.

The benchmark is a target which the fund seeks to achieve. The rate has been chosen as the fund’s benchmark as it is an achievable performance target and best reflects the scope of the fund’s investment policy.

The benchmark is used solely to measure the fund’s performance and does not constrain the fund's portfolio construction. The fund is actively managed. The investment manager has complete freedom in choosing which assets to buy, hold and sell in the fund.

Fund performance prior to 26 October 2018 refers to the UK-authorised OEIC, which merged into the M&G (Lux) Episode Macro Fund (a Luxembourg-authorised SICAV) on 26 October 2018. Tax rates and charges may differ.

The fund allows for the extensive use of derivatives.

Investing in this fund means acquiring units or shares in a fund, and not in a given underlying asset such as a building or shares of a company, as these are only the underlying assets owned by the fund.

Further risks associated with the fund can be found in the fund’s Prospectus.

[1] “Active asset allocation more important than ever,” February 2021. “The importance of flexibility,” July 2022.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.