Pursuing long-term growth and thematic tailwinds

6 min read 27 Jun 23

The value and income from the fund's assets will go down as well as up. This will cause the value of your investment to fall as well as rise and you may get back less than you originally invested. There is no guarantee that the fund will achieve its objective and you may get back less than you originally invested. Past performance is not a guide to future performance.

We remain undeterred in our pursuit of long-term growth in an asset class exposed to multiple thematic tailwinds. Renewable energy, digital connectivity and demographics, to name but a few, are powerful, enduring themes, which we believe will support strong growth for many decades to come.

Market environment YTD

Despite ongoing concerns about persistent inflation, rising interest rates and the prospect of a recession, equity markets have confounded the sceptics with a strong rally, albeit confined to a select few sectors. The dominance of technology and the new economy has left everything else in its wake, creating a difficult environment for anything other than growth-focused portfolios exposed to a narrow field of winners. Champions of the digital era, particularly those associated with artificial intelligence (AI), hogged the limelight. NVIDIA’s guidance exceeded the most bullish of expectations, but the euphoria has also rekindled more worrying elements of investor behaviour. Speculation is back, with the GS Non-Profitable Tech Index (also referred to as the “negative earnings” company index among market participants) up 15% in May.

The style rotation away from value and defensives, which proved resilient in 2022, towards growth, which flourished during the halcyon days of low growth and low interest rates, has provided a significant headwind for listed infrastructure as an asset class. Utilities, which typically dominate listed infrastructure portfolios, have declined in a rising market as investors shun perceived sensitivity to changes in interest rates.

Fund performance

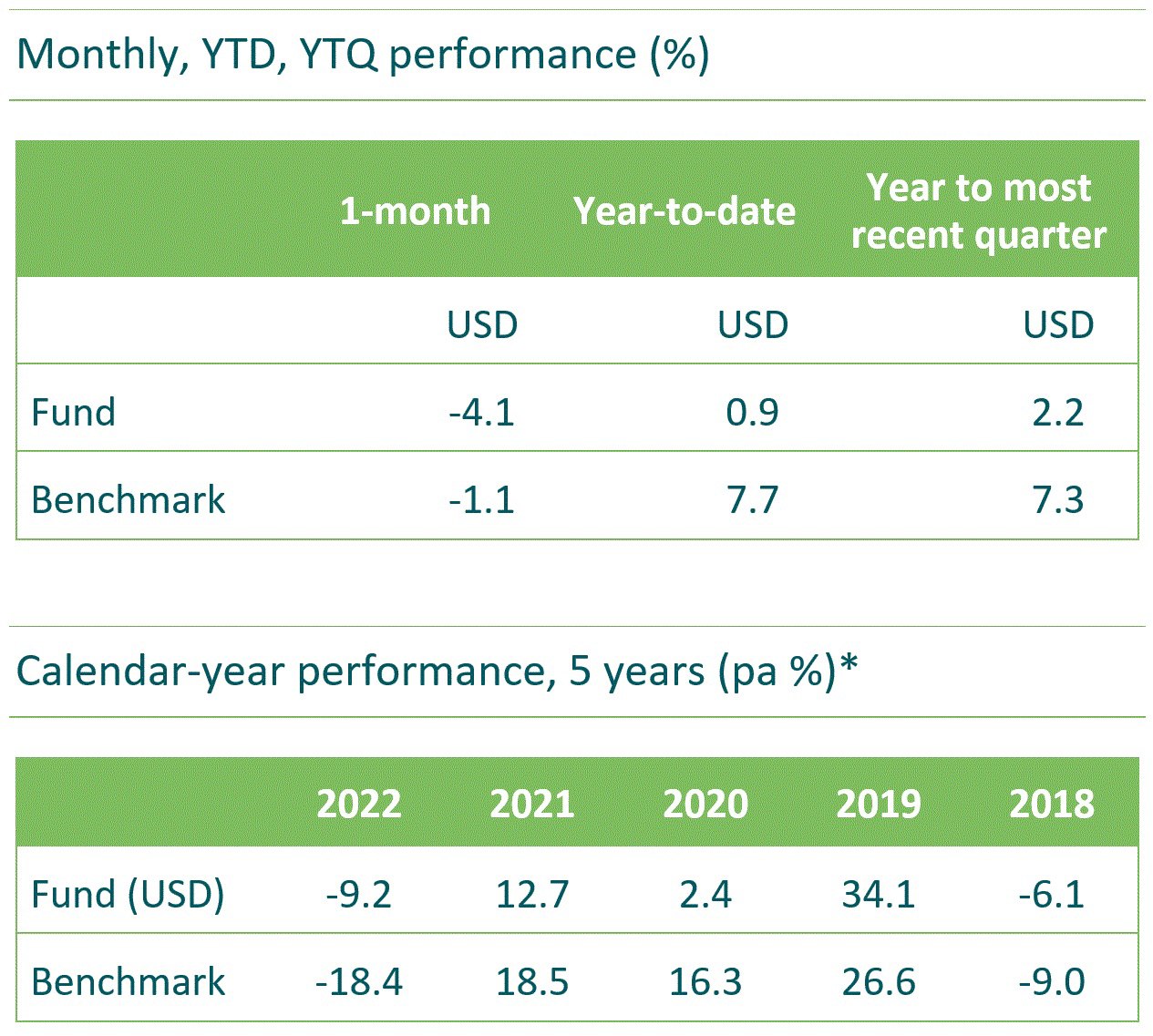

The M&G (Lux) Global Listed Infrastructure Fund has generated a positive return this year, but has underperformed the MSCI ACWI Net Return Index, against a challenging backdrop for listed infrastructure. The likes of NVIDIA, Microsoft, Apple and Meta Platforms are simply not infrastructure businesses and are therefore ineligible for our strategy.

The fund compares more favourably in a listed infrastructure context. The fund has outperformed the average in the Morningstar Sector Equity Infrastructure Sector and ranks second quartile (40th percentile) in the peer group.

Past performance is not a guide to future performance.

Source: Morningstar Inc., 31 May 2023, USD A class shares, income reinvested, price to price.

The fund’s benchmark is the MSCI ACWI Net Return Index. The benchmark is a comparator against which the fund’s performance can be measured. It is a net return index which includes dividends after the deduction of withholding taxes. The index has been chosen as the fund’s benchmark as it best reflects the scope of the fund’s investment policy. The benchmark is used solely to measure the fund’s performance and does not constrain the fund's portfolio construction. The fund is actively managed. The investment manager has complete freedom in choosing which investments to buy, hold and sell in the fund. The fund’s holdings may deviate significantly from the benchmark’s constituents. The benchmark is not an ESG benchmark and is not consistent with the ESG Criteria and Sustainability Criteria.

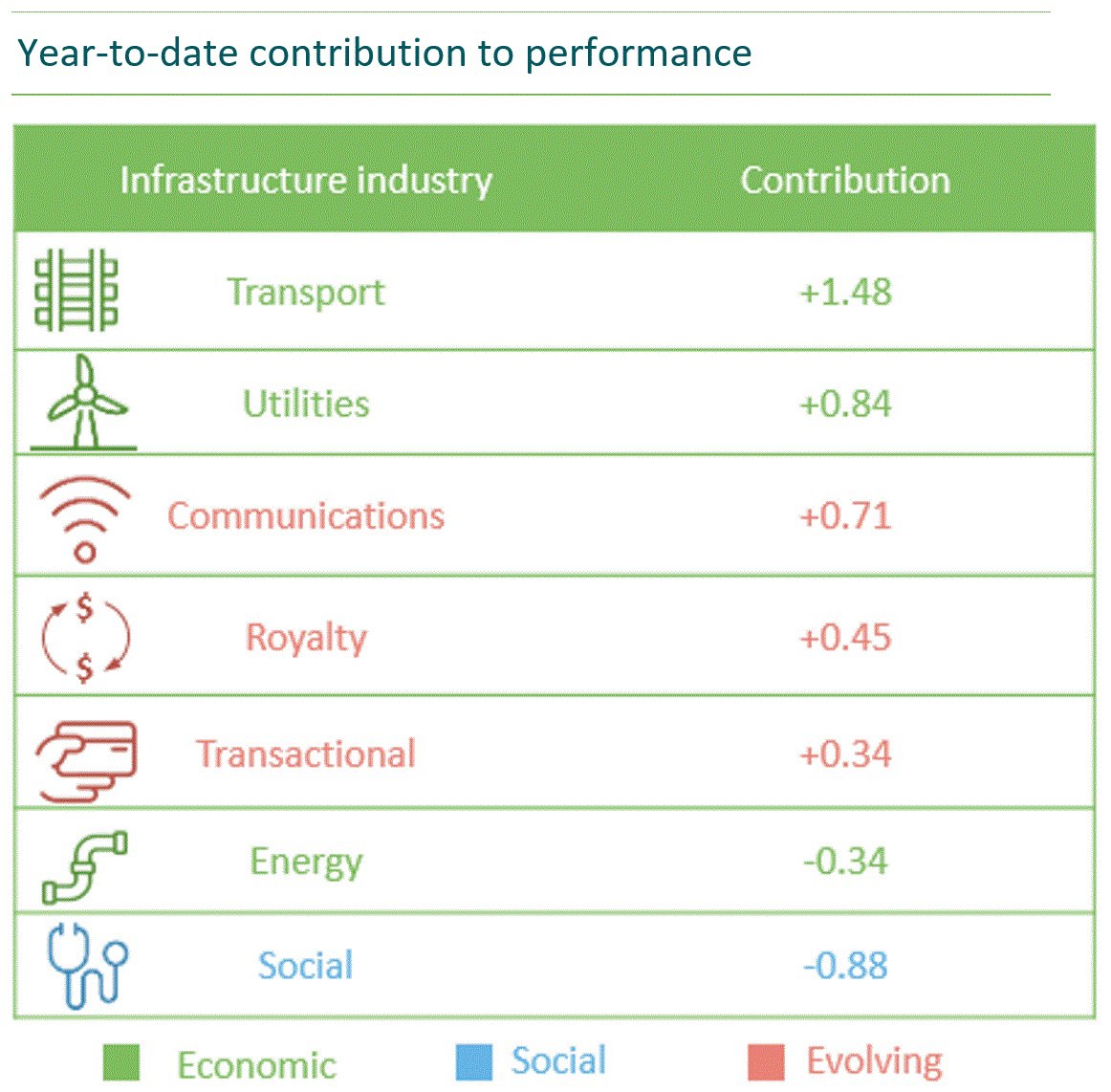

Our holdings in transportation infrastructure added the most value in the year to the end of May, as Vinci, CCR and Ferrovial delivered double-digit returns. E.ON, Enel and A2A rallied strongly in European utilities, in contrast to AES Corp, Eversource Energy and NextEra Energy Partners, which declined in the US. In communications infrastructure, Infrastrutture Wireless Italiane (INWIT) rose on takeover talk. Equinix’s gain was backed by solid fundamentals as the data centre company reported better-than-expected results for the first quarter and raised its outlook for the year.

Source: M&G, as at 31 May 2023

‘Social’ infrastructure provided the biggest drag on fund performance, not helped by the weakness in Alexandria Real Estate. Perceived interest-rate sensitivity weighed on a variety of holdings structured as real estate investment trusts (REITs), but to us the long-term investment case remains intact. We continue to have confidence in Alexandria Real Estate, which provides exposure to life science infrastructure, and in its ability to generate reliable and growing cashflows from unique assets, which are critical to the research and development of drugs to address society’s ongoing medical needs. We added to the holding on weakness.

ONEOK and Gibson Energy fell in line with an out-of-favour energy sector. As is the case for our other holdings in energy infrastructure, we remain convinced of the critical importance of pipelines, storage terminals and processing facilities, and the crucial role these strategic assets play in the smooth functioning of the global economy. ONEOK and Gibson remain attractively valued, in our opinion, on dividend yields of more than 6%.

Listed infrastructure and perceived interest-rate sensitivity

The increasing likelihood of interest rates remaining higher for longer has prompted investors to reassess their views on leverage. An indiscriminate selloff in more indebted businesses ensued, with real estate and utilities bearing the brunt of negative sentiment. It is true that infrastructure businesses can accommodate higher levels of debt given the reliable and growing cashflows generated from critical assets, but their capacity for debt is not limitless.

Balance sheet strength is a key consideration in our fundamental analysis, to avoid the damaging consequences of excessive leverage. It is worth highlighting that many of our holdings, particularly those in the ‘evolving’ segment, carry net cash on their balance sheet – a unique characteristic that we believe sets us apart from traditional infrastructure strategies.

Balance sheet analysis for infrastructure businesses is riddled with complexity. Many companies, particularly those in utilities and transportation infrastructure, issue debt at the asset level rather than the corporate level, which can mask higher intrinsic levels of balance sheet leverage. We monitor these details on a stock-by-stock basis.

That said, the M&G (Lux) Global Listed Infrastructure Fund’s disciplined and meticulous approach to leverage is reflected in debt levels which have been consistently lower than those of the asset class overall. The fund’s net debt/EBITDA ratio is estimated to be just below 3.5x, compared to 5.9x for the FTSE Global Core Infrastructure 50/50 Index, which is representative for the asset class. Stress tests provided by the risk team on the leverage factor also demonstrate that the fund would be less impacted than listed infrastructure indices in a scenario where more indebted companies are penalised. We remain committed to scrutinising the balance sheet strength of each company in which we invest.

Structural growth opportunities (including the energy transition)

The M&G (Lux) Global Listed Infrastructure Fund remains undeterred in its pursuit of long-term growth in an asset class exposed to multiple thematic tailwinds. Renewable energy, digital connectivity and demographics, to name but a few, are powerful enduring themes, which we believe will support strong growth for many decades to come.

The energy transition, in particular, is a theme that features prominently in the fund, our conviction endorsed by government policies and incentives aimed at addressing climate change. The increasing incidence of extreme weather events such as floods, hurricanes and forest fires, and the devastation they bring to communities and economies, provide a telling reminder that the task is urgent. Infrastructure is widely acknowledged as central to the long-term solution, with utilities playing a pivotal role in the development of renewables, including new sources of clean energy such as green hydrogen, and the development of smart grids and low voltage networks in transmission and distribution, respectively. We believe that the tailwind for infrastructure is here to stay.

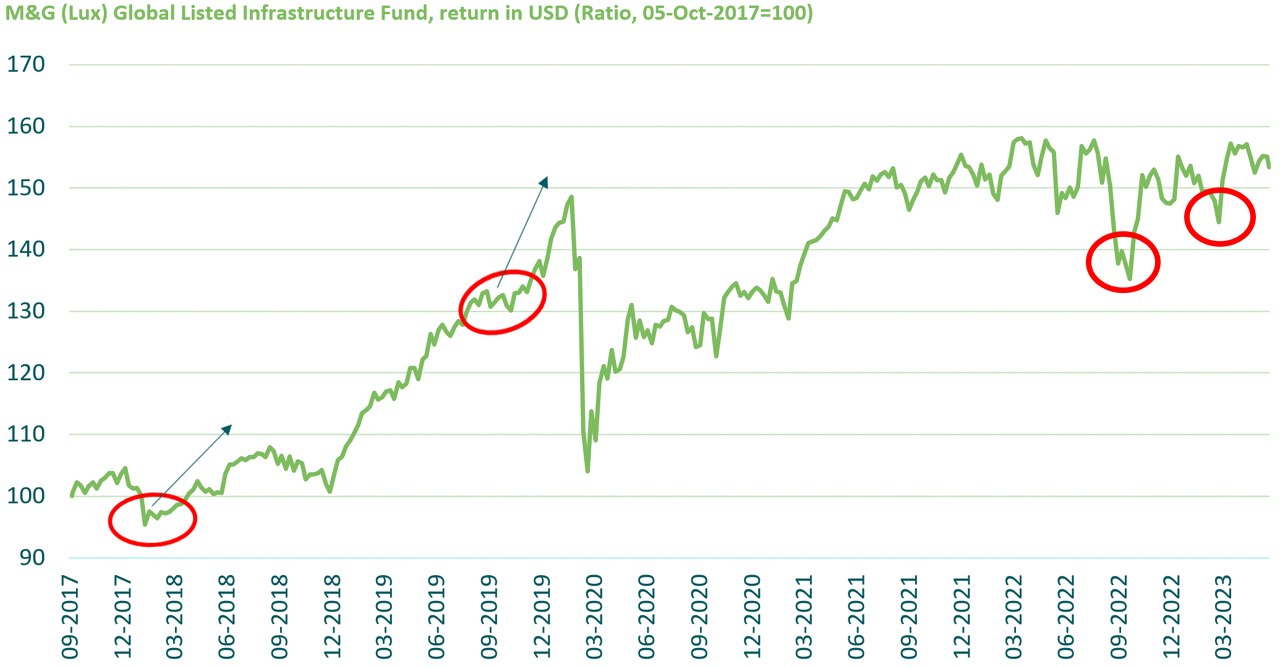

Source: Datastream, 21 June 2023. Rebased to 100 at 5 October 2017. USD A Acc shares, income reinvested, price to price.

The market’s tendency to be swayed by macroeconomic fears can present excellent buying opportunities for long-term growth companies. We see the current aversion to perceived interest-rate sensitivity as another attractive entry point.

Crown Castle and American Tower, both communications towers companies, have succumbed to downward pressure owing to their status as REITs. But their sector classification belies strong growth credentials driven by technological developments in the new economy. To us, from a fundamental perspective, the long-term investment case for both companies remains robust. We remain as optimistic as ever about the prospects for structural growth in digital infrastructure, as the long-term trend of rising mobile penetration and data usage globally continues to gather momentum. We added to these core holdings on weakness.

In the ‘evolving’ category of infrastructure, where growth characteristics are most pronounced, communications infrastructure accounts for 18% of the fund by weighting, compared to a typical range of 10-20%, while transactional infrastructure, which includes the owners and operators of physical networks that enable digital transactions, accounts for another 5%.

We believe that the fund is well placed, owing to the actions we have taken, and we are confident that performance can recover from its recent bout of volatility. We have experienced similar periods of nervousness about the path of interest rates in the past. On each occasion, we have acted with conviction by buying into weakness and were subsequently rewarded with bursts of strong performance. We expect the current circumstances to be no different. Past performance is not a guide to future performance.

Outlook

We are under no illusion about the uncertainties in the global economy, but we are as excited as ever about the long-term opportunities in listed infrastructure. In our opinion, the asset class offers defensive characteristics in the event of a recession, and provides inflation protection by way of index-linked revenue while central banks grapple with the challenge of keeping inflation in check. But the attractions of listed infrastructure’s reliable and growing cashflows have considerable appeal beyond the current environment. Listed infrastructure is a beneficiary of structural trends, which we believe will provide ample growth opportunities for investors with a long-term time horizon.

From an investment standpoint, we take comfort from the abundance of attractive ideas from a bottom-up perspective. Being selective will be paramount in these volatile times. Valuation is a key consideration in the stock selection process, and we see plenty of long-term growth opportunities without having to overpay for the privilege.

We initiated a new holding for the first time in a year with the new purchase of Kamigumi, our first investment in Japan. The country’s largest port operator has demonstrated a strong commitment to shareholder returns by way of dividends and share buybacks, supported by what we see as a rock-solid balance sheet with net cash. The potential to realise value from its non-core assets offers further upside for a stock trading on an undemanding valuation. With more potential investment candidates in the pipeline, we remain optimistic about the long-term prospects for our growth-focused strategy.

Past performance is not a guide to future performance.

*As the fund launched on 5 October 2017, we are unable to show 10 years of performance data.

Benchmark = MSCI ACWI Net Return Index.

The benchmark is a comparator against which the fund’s performance can be measured. It is a net return index which includes dividends after the deduction of withholding taxes. The index has been chosen as the fund’s benchmark as it best reflects the scope of the fund’s investment policy. The benchmark is used solely to measure the fund’s performance and does not constrain the fund's portfolio construction.

The fund is actively managed. The investment manager has complete freedom in choosing which investments to buy, hold and sell in the fund. The fund’s holdings may deviate significantly from the benchmark’s constituents. The benchmark is not an ESG benchmark and is not consistent with the ESG Criteria and Sustainability Criteria.

Source: Morningstar, Inc., as at 31 May 2023, USD Class A Acc shares, income reinvested, price-to-price basis. Benchmark returns stated in share class currency.

The main risks associated with this fund:

- The fund can be exposed to different currencies. Movements in currency exchange rates may adversely affect the value of your investment.

- Investing in emerging markets involves a greater risk of loss due to greater political, tax, economic, foreign exchange, liquidity and regulatory risks, among other factors. There may be difficulties in buying, selling, safekeeping or valuing investments in such countries.

- The fund holds a small number of investments, and therefore a fall in the value of a single investment may have a greater impact than if it held a larger number of investments.

- In exceptional circumstances where assets cannot be fairly valued, or have to be sold at a large discount to raise cash, we may temporarily suspend the fund in the best interest of all investors.

- The fund could lose money if a counterparty with which it does business becomes unwilling or unable to repay money owed to the fund.

Other important information:

- Please note that the fund invests mainly in company shares and is therefore likely to experience larger price fluctuations than funds that invest in bonds and/or cash.

- Investing in this fund means acquiring units or shares in a fund, and not in a given underlying asset such as a building or shares of a company, as these are only the underlying assets owned by the fund.

- For explanation of technical terms, please refer to the glossary via the link https://docs.mandg.com/docs/glossary-master-en.pdf

- Further risk factors that apply to the fund can be found in the fund's Prospectus.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

M&G Investments does not provide any asset management service in Hong Kong. This website is general in nature and is for information purposes only. It is not a solicitation, offer or recommendation of any security, investment management or advisory service. The information on this website is for Professional Investors only. Specifically, the information on these pages should not be used or relied upon by the public of Hong Kong or any other type of investor from any other jurisdiction.

This website has been issued by M&G Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission.