|

MSCI World Growth Index Weight % |

MSCI World Index Weight % |

YTD Perf % |

Apple |

10.16 |

4.93 |

51.6 |

Microsoft |

7.76 |

4.07 |

40.7 |

Amazon |

4.03 |

2.28 |

59.1 |

Nvidia |

3.77 |

1.95 |

219.8 |

Alphabet A |

2.58 |

1.36 |

50.4 |

Tesla |

2.49 |

1.25 |

117.1 |

Alphabet C |

2.34 |

1.23 |

50.0 |

Meta |

2.31 |

1.22 |

164.8 |

Visa |

1.26 |

0.68 |

14.4 |

Eli Lily |

1.20 |

0.63 |

25.0 |

Total |

37.91 |

19.60 |

|

Value

Was it really one and done for Value?

6 min read 12 Sep 23

Summary: The re-emergence of Value in 2022 after more than a decade in the doldrums provided hope that this momentum could be sustained into the years that followed. While at a headline level this hope now looks like a fond illusion, a deeper look reveals what we believe to be strong evidence that the long-awaited renaissance of Value is in fact ongoing in many global markets.

The value and income from the fund's assets will go down as well as up. This will cause the value of your investment to fall as well as rise. There is no guarantee that the fund will achieve its objective and you may get back less than you originally invested. Past performance is not a guide to future performance. The views expressed in this document should not be taken as a recommendation, advice or forecast.

Back to the future for Growth?

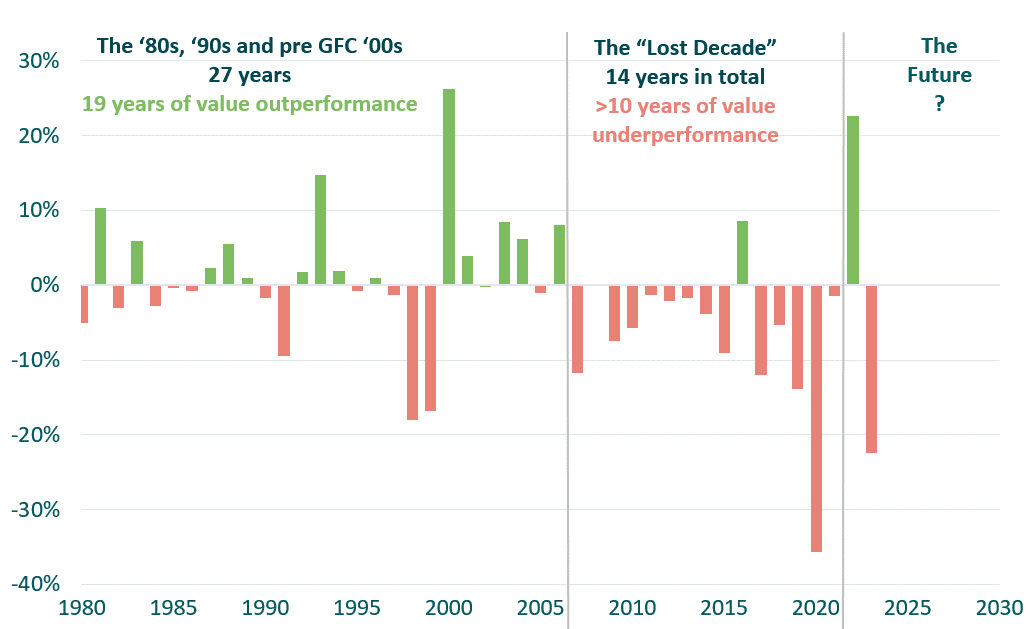

At a headline level, the performance of Value versus Growth (see Figure 1) leaves the stark impression that 2022 was little more than a brief aberration. After it passed, the prevailing trends of the past decade seem to have been re-established and any sparks of regime change extinguished.

There is no questioning that at an index level the differentials between Growth and Value in the first seven months of the year have been significant. The MSCI World Value index has delivered a respectable 8% return, but that is dwarfed by the 31% return achieved by the MSCI World Growth index, with this being achieved in an environment where interest rates have continued to rise in most developed countries.

Figure 1: MSCI World Value vs Growth

Past performance is not a guide to future performance

Source: MSCI, as at 31 July 2023, USD denominated

So what’s driving this stellar return for Growth? Are we experiencing a return to the trends we’ve seen in the past few years, or is it something new? Looking at the breadth and composition of returns driving Growth indices, the trends we see don’t suggest we’re back to the “nothing but Growth” era. Instead, what we are seeing is a continued narrowing in the breadth of stocks positively contributing to the style. This effect has so far been materially offset by outsized returns from a select few stocks, which also dominate due to their size in the overall index.

Much has been written on the narrowness of returns this year, notably in the US, and this effect is being amplified when we look at the construction of Growth indices. The top 10 names in the MSCI World Growth index now account for just under 40% of the total index and almost 20% of the broader MSCI World Index (see Figure 2). These 10 stocks have also delivered on average a staggering year-to-date return of 79%, leaving little for the rest of the universe to contribute.

Past performance is not a guide to future performance.

Figure 2: The top 10 names that dominate the indices

Source: MSCI, 31 July 2023

Growth turns to Value, then back to Growth

Another interesting feature of the Growth index is the inclusion of certain stocks. The labelling of stocks into either Value or Growth camps is an endless debate. However, it is interesting to note that both Meta and Alphabet, two of the largest stocks in the MSCI World Growth index, have been Value index constituents throughout 2023. In the case of Meta, the material de-rating it experienced over the past 18 months saw it trading at close to 10x forward earnings – a multiple where it’s difficult to argue that it didn’t represent fantastic value.

Alphabet is a similar example; the stock was trading at more than two standard deviations below its long-term average earnings multiple by mid-January, before performing very strongly. Maybe there’s an argument that some of the success of Growth so far this year has been borrowed from Value?

The Value renaissance continues

Although the headline numbers suggest Value has once again been consigned to the dustbin, the deeper we look, the more we find evidence that this isn’t the case.

Putting aside the inherent biases and nuances that come with index construction and instead focusing on pure factors, we see a very different picture in the performance of Value relative to Growth (See Figure 3). Value, far from being left behind, leads Growth in most markets outside the US, in some cases by a substantial margin.

Figure 3: Bloomberg Factor performance – long / short, sector neutralised, equally weighted portfolios

Factor |

S&P 500 Index |

STOXX Europe 600 Index |

TOPIX Index |

Bloomberg Emerging Markets Index |

Growth |

5.95 |

-1.32 |

-7.07 |

-6.11 |

Value |

-5.90 |

4.75 |

19.14 |

11.21 |

Source: Bloomberg, 18 August 2023

Japan, long seen as one of the great value traps, has been a standout performer for the style. We have seen an increasing awareness and action by Japanese companies to improve corporate governance and shareholder returns for some time. In addition to that, an announcement in February by the Tokyo Stock Exchange encouraging companies (especially those trading at less than 1x price to book) to increase their focus on sustainably improving returns has provided even more impetus for the pace of change to accelerate. The fact that roughly half the Japanese market is currently trading below the 1x price to book threshold hasn’t been lost on global investors.

Although Japan has been a standout performer for Value, it has been well supported by other regions. Whilst the sharp rise in the cost of capital experienced during 2022 provided the catalyst for Value’s turnaround, in our view this turnaround has also been supported by a number of other drivers, some of which were either emerging or have accelerated since the pandemic.

Whether it be the acceleration of the global energy transition driven by US incentives, Russia’s war on Ukraine, China’s attempts to re-structure its property market or the uneven exit of economies from the COVID pandemic, these factors are helping to drive a change in the relative attractiveness of many stocks.

Whereas for much of the past decade we have seen a high level of singularity in the drivers of performance across and within global equity markets, today we see multiple dislocations. We believe this is creating a broader base of opportunities from which to generate alpha, and therefore helping to level the playing field for active Value investors in trying to offset the outsized performance from a concentrated number of mega-cap Growth stocks.

Will the impending recession derail Value?

As interest rates continued to fall for much of the last decade, supported by a narrative of secular stagnation, investors’ perception of risk also changed relative to prior periods.

As a result, stocks perceived as either ‘Value’ or ‘high risk’ saw a change in their patterns of performance, exhibiting much larger drawdowns in periods of economic weakness, followed by stronger performance in periods of economic recovery.

Value has many defensive areas that historically have provided a buffer to cyclical Value stocks during periods of economic weakness. However, over the past decade this dynamic has not been strong enough to offset the performance of long duration Growth stocks, which have been supported by ever lower interest rates.

The normalisation of interest rates that has occurred over the past year, back to levels not seen for the last decade (and at a time when valuation dispersions remain at or close to historical highs) provides, in our opinion, the potential for the natural diversification that exists within Value to play a more dominant role.

Whilst we could argue that many cyclical Value stocks are already priced for a recession, we see the opportunity for defensive Value stocks to act not just as a natural hedge from any cyclical weakness, but also as a source of diversification should interest rates remain at more normalised levels, and we see valuation compression.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.