Monthly, YTD performance (%), Calendar year performance, 5 years (PA, %)

| 1-month | YTD | 2022 | 2021 | 2020 | 2019 | 2018 | |

|---|---|---|---|---|---|---|---|

| Fund | -4.3 | -7.4 | 3.3 | 15.4 | 1.3 | 31.4 | 1.1 |

| Benchmark | -0.4 | 8.9 | -7.6 | 20.1 | 13.2 | 22.4 | -3.3 |

Equities

10 min read 19 Oct 23

The value and income from the fund's assets will go down as well as up. This will cause the value of your investment to fall as well as rise. There is no guarantee that the fund will achieve its objective and you may get back less than you originally invested. Past performance is not a guide to future performance. The views expressed in this document should not be taken as a recommendation, advice or forecast.

Listed infrastructure as an asset class has been under severe pressure. Utilities, closely followed by real estate, have been the worst performing sectors this year, owing to their perceived sensitivity to changes in interest rates. The underperformance relative to the broader market has been extreme, even in a historic context. Global utilities are experiencing their worst period of relative performance since the financial crisis, and US utilities are suffering their worst performance since 1999 during the tech bubble.

Figure 1: Market environment in 2023 YTD: The dominance of tech and the new economy

Past performance is not a guide to future performance

Source: Aladdin, Bloomberg, 29 September 2023

The negative sentiment towards the asset class, which has intensified during August and September, is reflected in the performance of the M&G Global Listed Infrastructure Fund, which has underperformed the MSCI ACWI Index year-to-date.

Relative to its peers, however, the fund has outperformed the IA Infrastructure sector, helped by a structural underweight in utilities. The fund typically has 20-40% in utilities compared to 50% or more for listed infrastructure peers and listed infrastructure indices. However, with more than 30% of the portfolio in utilities, the fund has struggled to offset the broader asset class effect in its entirety.

Stock selection has also cushioned some of the blow. Despite a difficult backdrop for utilities overall, some of the fund’s European utility holdings (A2A, Enel and E.ON) have been the biggest positive contributors to performance this year (to end-September).

In September, the fund’s performance was affected by a company-specific issue with NextEra Energy Partners, which lowered its dividend growth guidance owing to the burden of higher interest rates. Parent company NextEra Energy fell in sympathy despite reaffirming its dividend growth target of 10%. Both companies play a pivotal role in the energy transition and to us, the long-term investment case remains intact.

Social and communications infrastructure holdings have also held back fund performance this year, owing to the weakness of companies structured as real estate investment trusts (REITs). Alexandria Real Estate, which owns and operates life science infrastructure, has borne the brunt of negative sentiment in social infrastructure, while the towers companies Crown Castle and American Tower led the laggards in communications infrastructure.

Our conviction in these core holdings remains intact. We continue to have confidence in the reliable and growing cashflows from Alexandria’s unique assets, which are critical to the research and development of drugs to address society’s ongoing medical needs. In communications infrastructure, we continue to see Crown Castle and American Tower as prime beneficiaries of the structural growth in digital infrastructure. We added to all three holdings on weakness.

Figure 2: Performance in 2023 YTD

Source: Morningstar Inc., UK database 29 September 2023, sterling I class shares, income reinvested, price to price.

Past performance is not a guide to future performance.

Monthly, YTD performance (%), Calendar year performance, 5 years (PA, %)

| 1-month | YTD | 2022 | 2021 | 2020 | 2019 | 2018 | |

|---|---|---|---|---|---|---|---|

| Fund | -4.3 | -7.4 | 3.3 | 15.4 | 1.3 | 31.4 | 1.1 |

| Benchmark | -0.4 | 8.9 | -7.6 | 20.1 | 13.2 | 22.4 | -3.3 |

Benchmark = MSCI ACWI Index

The benchmark is a target which the fund seeks to outperform. The index has been chosen as the fund’s benchmark as it best reflects the scope of the fund’s investment policy. The benchmark is used solely to measure the fund’s performance and income objective and does not constrain the fund's portfolio construction.

The fund is actively managed. The fund manager has complete freedom in choosing which investments to buy, hold and sell in the fund. The fund’s holdings may deviate significantly from the benchmark’s constituents.

Source: Morningstar, Inc., as at 30 September 2023, GBP Class I Acc shares, income reinvested, price-to-price basis. Benchmark returns stated in share class currency.

Figure 3: Utilities and real estate – Distressed valuation

Source: Datastream, 29 September 2023

The market’s panicky reaction to perceived interest rate sensitivity has been extremely frustrating, but fear creates opportunity. We strongly believe that today’s valuation levels present a highly attractive entry point for long-term investors.

The MSCI ACWI Utilities Index and the MSCI ACWI Real Estate Index are trading at their cheapest levels since the global pandemic, after which time both sectors were re-rated upwards significantly.

This valuation support gives us confidence that the asset class can recover from its recent bout of volatility. We have experienced similar periods of market nervousness in the past. On each occasion, we have acted with conviction by buying into weakness where we believe the long-term growth opportunity remains intact, and were subsequently rewarded with bursts of strong performance.

We continue to see inflation-beating dividend growth across the portfolio, with the majority of holdings increasing their dividends in the core 5-10% range. But we are not resting on our laurels. We have been active in replacing companies exhibiting low dividend growth with new ideas delivering higher growth – high enough to offset the ravages of persistent inflation.

We divested CCR, the Brazilian toll road operator, owing to concerns about the lack of dividend growth, and we have earmarked others for the same treatment on the same grounds.

We are also delighted with the quality of investment opportunities available in the current market environment. The recent purchases of Kamigumi, the Japanese ports company, and Getlink, the owner and operator of Eurotunnel, provide a case in point. Both companies are not only proud owners of unique, critical infrastructure -- they also boast strong shareholder value credentials by way of impressive dividend growth. Both stocks offer long-term attractions without having to overpay for the privilege.

Being selective will be paramount in these volatile times. With more potential investment candidates in the pipeline, we remain optimistic about the long-term prospects for the fund.

We strongly believe that the market’s aversion to perceived interest rate sensitivity provides an attractive entry point for a strategy capable of delivering real growth over the long term in excess of G7 inflation by way of growing dividends. The powerful tailwinds driving infrastructure are as robust as ever, in our view.

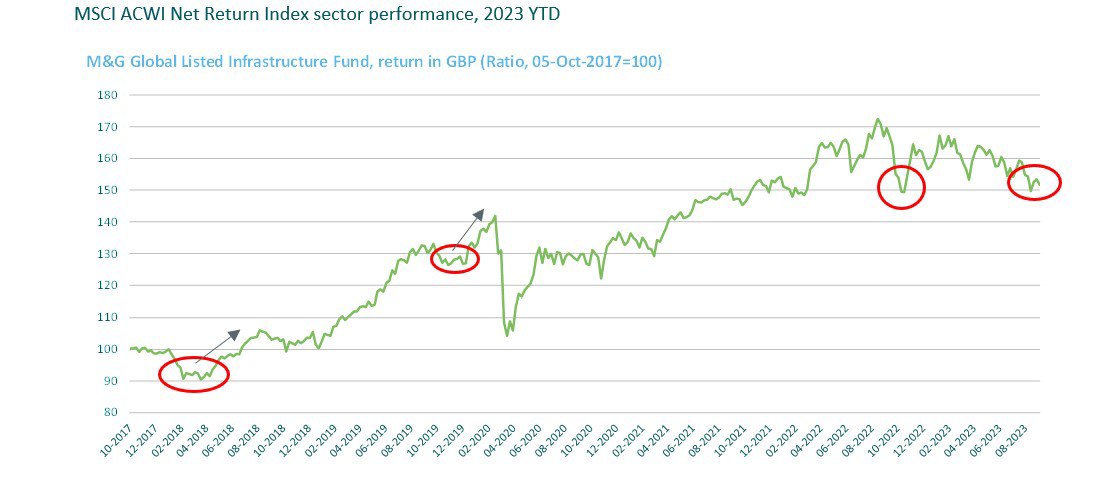

Figure 4: Interest rate-related volatility…can present opportunity

Past performance is not a guide to future performance

Source: Datastream, 8 September 2023. Rebased to 100 at 5 October 2017. Sterling I shares, price to price net income reinvested net of fees.

The energy transition, for example, is a theme that features prominently in the fund, our positive view endorsed by government policies and incentives aimed at addressing climate change. The Inflation Reduction Act (IRA) in the US has only been in effect for 12 months; the largest ever investment in clean energy and climate action has only just begun.

Since the IRA became law in August 2022, the US private sector has committed more than $110 billion in new clean energy manufacturing investments, including more than $70 billion in the electric vehicle (EV) supply chain and more than $10 billion in solar manufacturing. US electricity generation from wind is expected to triple and solar generation to increase as much as eight-fold by 20301 as the world’s leading economy aims to meet its climate goals, build a clean energy economy and strengthen energy security.

The ambitious programme is topical and timely. The increasing incidence of extreme weather events and the havoc they bring to communities around the world provide a constant reminder that the task is urgent. The devastating wildfires in Hawaii remain etched in our memories, but provide just one example in a long list of many.

Infrastructure is widely acknowledged as central to the long-term solution to climate change, with utilities playing a pivotal role in the development of renewable energy sources, the reconfiguration of grids to accommodate new sources of energy, and the development of low-voltage networks fit for the modern age. We believe the tailwind for infrastructure is here to stay.

We remain resolute in our pursuit of long-term growth opportunities, which in our opinion are abundant across the asset class. Six years into our listed infrastructure journey, our conviction has never been stronger.

The main risks associated with this fund:

Other important information:

Please note that the fund invests mainly in company shares and is therefore likely to experience larger price fluctuations than funds that invest in bonds and/or cash.

Further risk factors that apply to the fund can be found in the fund's Prospectus.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.