Consumer Duty

Consumer Duty - What advisers really think

4 min read 16 Feb 23

If you needed any convincing about how seriously the FCA wishes you to take its Consumer Duty rules you should know it has taken to podcasts to explain them. At the time of writing it had tackled three of the Duty’s four outcomes and they are well worth a listen.

Time is of the essence. Now that we are well into 2023, the regulator’s 31 July deadline for implementation of the Consumer Duty for new and existing products and services will be here before we know it (closed products get a further year).

So, how are advice firms’ plans going? Are advisers expecting the Duty’s outcomes to make the differences the FCA hopes they will? And, with the FCA already reviewing larger ‘fixed’ firms’ progress, how and when will they assess smaller advice firms’ readiness?

Thankfully, because of our latest research into The State of the Adviser Nation 2023, we have some answers to these questions…

How ready are advisers for Consumer Duty?

The first thing you may wish to know is whether you are ahead, on par, or possibly behind your peers when it comes to Duty preparedness.

Well, the first thing we asked advice firms taking part in our study was how they felt their implementation plans were going. It’s worth pointing out the responses we received represent only a snapshot in time: they were given between October and November 2022, so a little time has passed and we expect plans to have advanced since then.

However, here is what they told us…

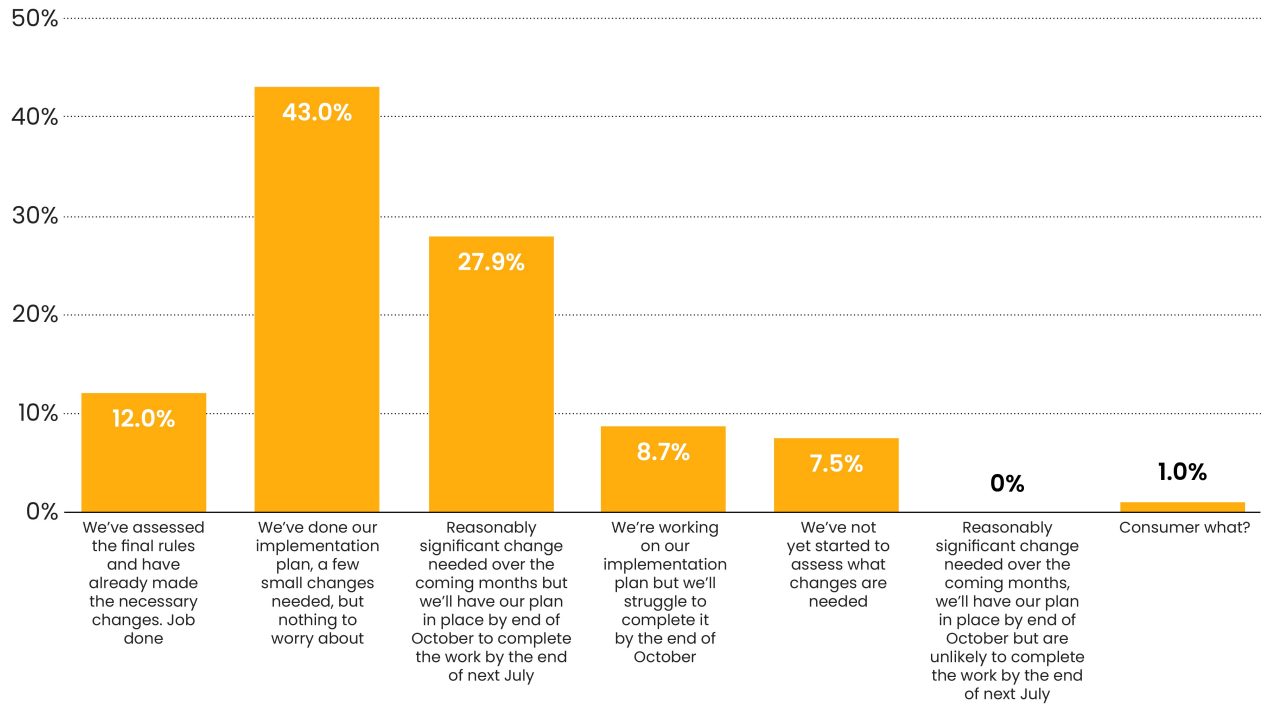

4.1 Which of these responses matches your firm regarding Consumer Duty?

Source: SOTAN, Jan 2023

On one end of the scale, 12% already felt it was ‘job done’ from their perspective. On the other, 7.5% confessed they hadn’t at the time done anything to prepare. Most firms, to varying degrees, feel they have everything in hand to meet July’s deadline. The largest single chunk of respondents said that, while their plans were not complete, only minor adjustments were needed.

We also asked firms for their views on each of the Duty’s four outcomes: value for money, consumer understanding; consumer support; and products and services. Here is what we learned…

Value for money

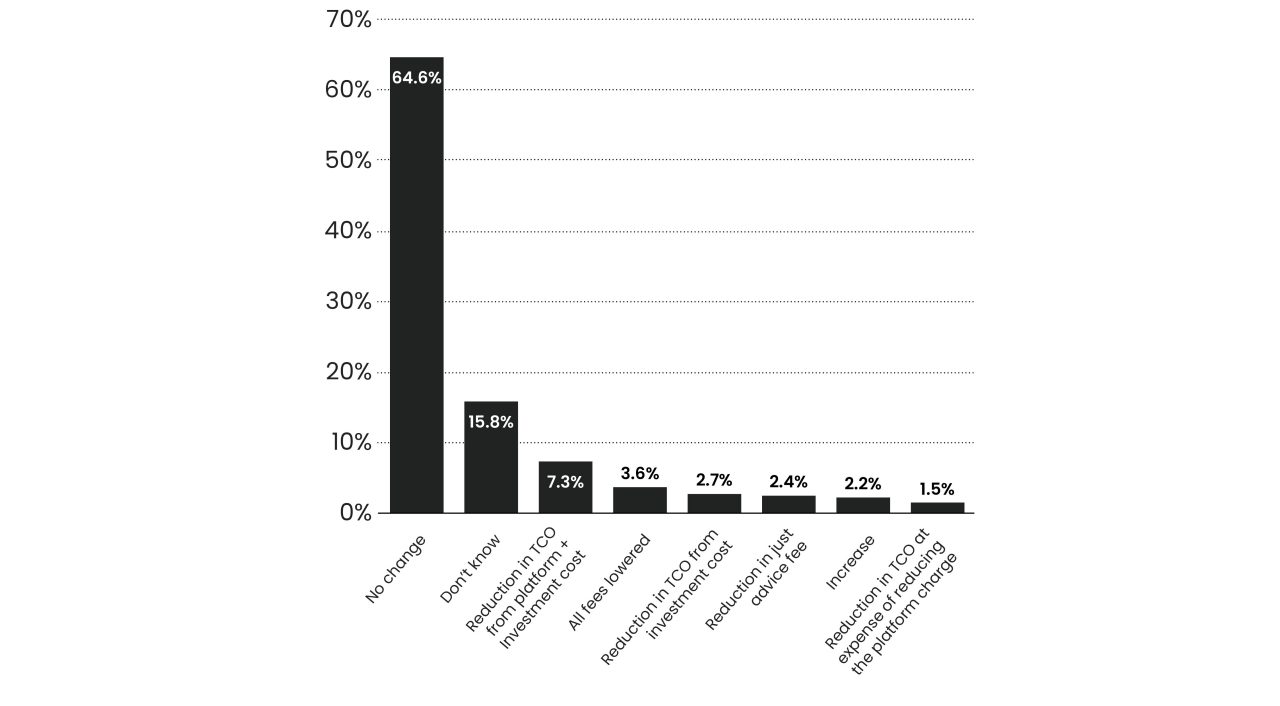

The Consumer Duty requires firms to ensure their products or services represent value for money. Advisers must carry out this assessment for their own advice fees, as well as on the total charge the client is paying. The FCA expects this outcome to have an impact in lowering costs for consumers.

With this increased focus on costs and value (and yes, they are two very different things) it is perhaps surprising to see two-thirds of respondents say there is likely to be no change in the level of charges consumers pay. Is this indicative of the fact advisers already focus on ensuring value for money for their clients? We think so...

4.2 Value for money assessments - what do you think it means for your clients?

Source: SOTAN, Jan 2023

Consumer understanding

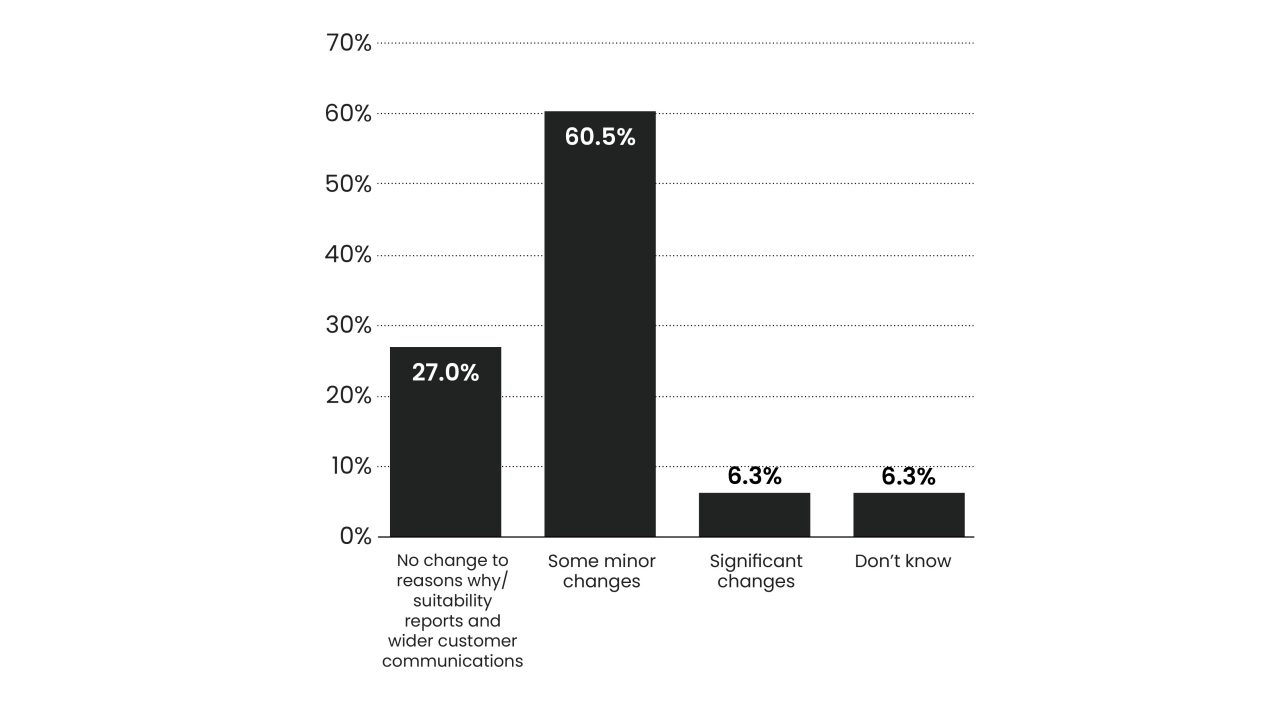

Advisers are clearly on the frontline when it comes to meeting the requirements of the consumer understanding outcome. They will know better than anyone how to communicate with clients. Consumer Duty will require firms to evolve these conversations, not only ensuring disclosures are ‘clear, fair and not misleading’ but also demonstrating that clients are able to make informed decisions as a result.

While a quarter of respondents are not anticipating making any changes, more than two-thirds expect some changes will need to be made. Again, this is one we expect will evolve over the coming months as firms move from planning mode to actual implementation.

4.3 What's the impact on your client communications?

Source: SOTAN, Jan 2023

Consumer support

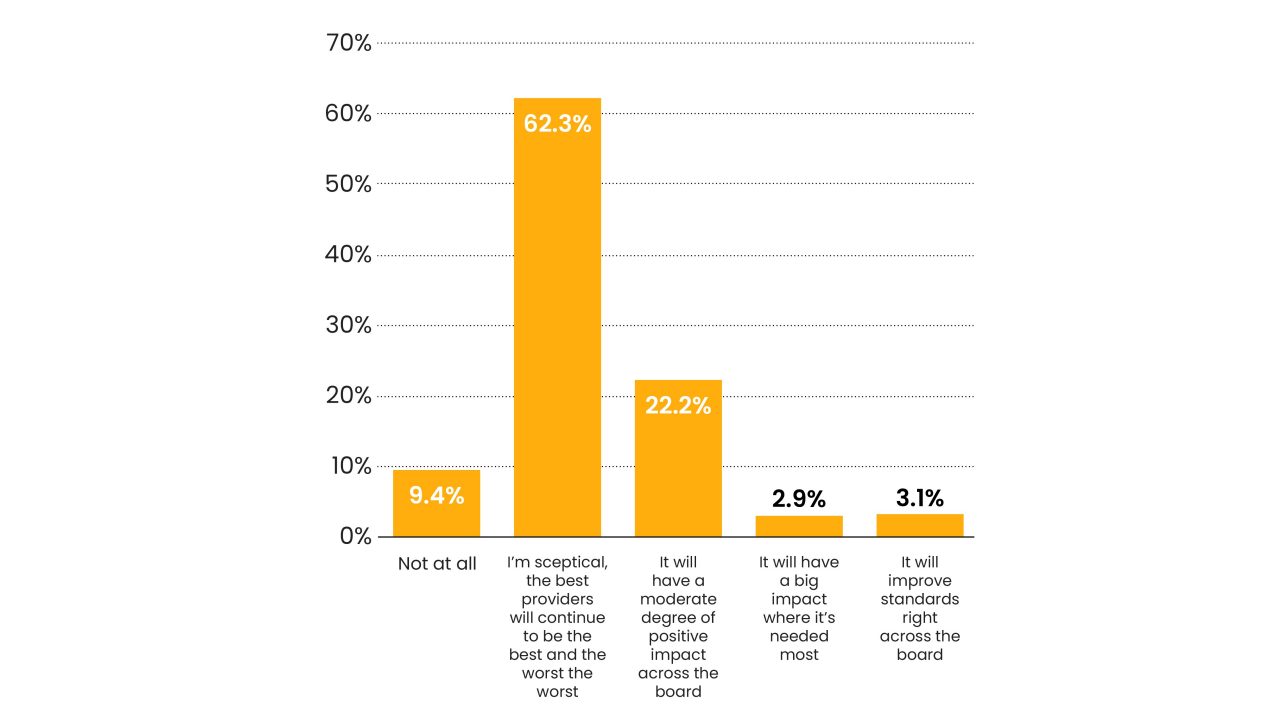

The consumer support outcome is another area where the FCA wants to see significant improvements.

Advisers tend to provide good standards of support directly to their own clients, so there is minimal direct impact on advice firms. There is, however, an increased requirement to assess providers’ support standards as part of their own research and due diligence.

Providers will need to ensure their service provision, both to advisers and consumers, meets the new standards. For some this will require significant effort – remodelling target operating models and SLAs – and the FCA hopes it will have a bumper impact on overall service standards.

Unfortunately, advisers don’t share the regulator’s optimism, with more 70% sceptical that improvements will be made.

Advisers will be delighted and will benefit considerably if there are indeed service improvements on the horizon, but they remain far from convinced this will be the case.

4.4 How do you think Consumer Duty will impact on provider service standards?

Source: SOTAN, Jan 2023

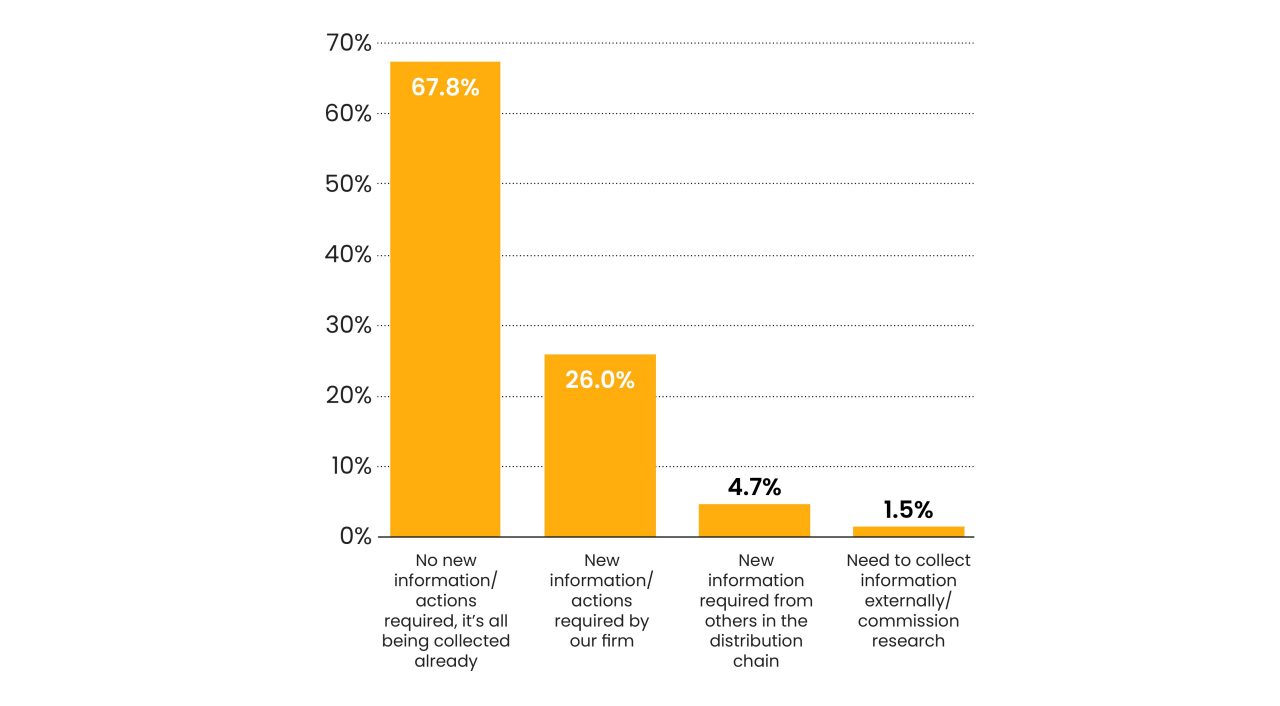

Products and services

The fourth Duty outcome requires firms to ensure their products and services have a clearly documented target market, with additional consideration of consumers in vulnerable circumstances.

This is an area where advisers feel they are already meeting the required standards, with two-thirds saying they already collect the necessary information. Some 26% of respondents anticipate they’ll need to change their current processes or collect extra information, either internally or from others.

4.5 How do you think Consumer Duty will change your approach to vulnerable customers?

Source: SOTAN, Jan 2023

What’s next – and the importance of prioritisation

That was a snapshot of what advice firms told us. So, what’s next?

In January, the FCA published the findings of its review into firm’s implementation plans. Its review focused on those larger ‘fixed’ firms with dedicated supervision teams – in other words the firms “with the greatest potential impact on consumers and markets”.

While the FCA praised some firms for embracing “the shift to focus on consumer outcomes” and said many were engaging well, it also identified plans that “suggested some firms may be further behind in their thinking and planning” than they would have preferred.

It’s advisers’ turn next. At some point in the coming weeks the FCA will be sending a survey to, and then conducting targeted engagements with, a sample of smaller firms to help it understand the progress they are making in implementing the Duty. This is likely to be with firms’ named consumer champion and will delve into how firms are dealing with vulnerable customers and how they are using client data, among other things. We’re unlikely to see the results until mid-March 2023 at the earliest.

Between its podcasts, webinars, letters, and other activity, there is a theme emerging: that the FCA is keen for firms to focus on prioritising where the greatest harm might be happening. So, whether you believe that lies with customer vulnerabilities, or broader client communications, prioritising your activities over the coming months, rather than trying to nail everything, may stand you in good stead.

Please note, the M&G Wealth Platform and its agents or representatives do not endorse or in any respect warrant any third party products or services by virtue of any advertisement, information, material or content referred to, or included on, or linked from or to this page.

The information contained in this page is for professional Financial Adviser use only. If you are a private investor, please visit the Private Investor section or contact your Financial Adviser for more information.