Pensions

Tax relief on employer pension contributions

Last Updated: 6 Apr 26 7 min read

Contents

1. Overview

2. Key Points

4. Corporate tax relief for pension contributions

Discover how an employer can receive tax relief on pension contributions for an employee.

Key Points

- Tax relief on employer contributions is given by allowing pension contributions to be deducted as a legitimate business expense.

- Deductions are only allowed in the chargeable period in which the contributions are paid.

- Large contributions can be spread over more than one period.

Corporation tax relief

Tax relief on employer contributions from companies is given against corporation tax. Partnerships and the self-employed who make pension contributions for their employees obtain tax relief through the contributions being deductible from their total profits.

See the corporation tax rates.

The tax treatment of employer pension contributions is significantly different to the tax treatment of member contributions.

Corporate tax relief for pension contributions

Since 6th April 2006 employers have been able to claim a deduction against corporation tax for unlimited sums paid to a registered pension scheme, provided they are paid 'wholly and exclusively' for the purposes of the employer's trade or business.

It goes without saying that to be able to receive an employer’s contribution, the individual needs to have an employer, so although the self-employed can pay employer’s contributions for their employees, they can’t make employer’s contributions for themselves. It's worth noting that the employer contributions made by the self-employed for their employees will not get corporation tax relief (as this doesn’t apply to the self-employed), but they do reduce the profits on which they have to pay tax.

Wholly and exclusively

Tax relief on employer contributions is given by allowing contributions to be deducted as an expense when calculating their profits.

In the case of:

- a trade or profession, employer contributions will be deductible as an expense provided that they are incurred wholly and exclusively for the purposes of the employer's trade or profession ICTA\S74(1)(a) - corporation tax and ITTOIA\S34 - income tax.

Part 2 of ITTOIA 2005

Part 3 of CTA 2009

- a company with investment business, the employer contributions will be deductible as an expense of management Chapter 2 of part 16 of CTA 2009.

Detailed guidance can be found in:

- Business Income Manual at BIM46000 onwards for trading employers.

- Company Taxation Manual at CTM08340 onwards for investment companies

The principles are perhaps best summed up by looking at extracts from the Business Income Manual:

.........the same rules apply as for any other expense .......... In particular, any contribution must be paid wholly and exclusively for the purposes of the trade for it to be deductible (ICTA88/S74 (1) (a) for corporation tax and ITTOIA05/S34 for income tax) ..........

..........it is important to emphasise that as part of the cost of employing staff pension contributions will, prima facie, be allowable ..........

..........Whether there was a non-trade purpose for the payment will depend upon the facts of the individual case ..........

..........One situation .......... is where the level of the remuneration package is excessive for the value of the work undertaken ..........

.......... accept that the contributions are paid wholly & exclusively .......... where the remuneration package paid in respect of a director of a close company, or an employee who is a close relative or friend of the director or proprietor (where the business is unincorporated) is comparable with that paid to unconnected employees performing duties of similar value ..........

The accountant is best placed to give a view and they can take the matter up directly with the HMRC officer dealing with the company's tax return.

Business Income Manual at BIM 46000

Tax relief – meaning of paid and chargeable periods

Deductions are only allowed in the chargeable period in which the contributions are paid.

For an employer pension contribution to be paid it must have actually been paid with the money cleared; having an 'accounting entry' i.e. an accrued liability for the payment, is not sufficient.

The companies equivalent of an individual's tax year is the 'financial year' which runs 1 April to 31 March (any change to corporation tax rates will usually be applied from 1 April).

The chargeable period is normally 12 months and is, basically, the company's financial year.

Chargeable periods do not need to follow the statutory financial year. Many companies use the financial year, while others follow the calendar year or some other period.

The rate of relief depends on the financial years covered by the chargeable period.

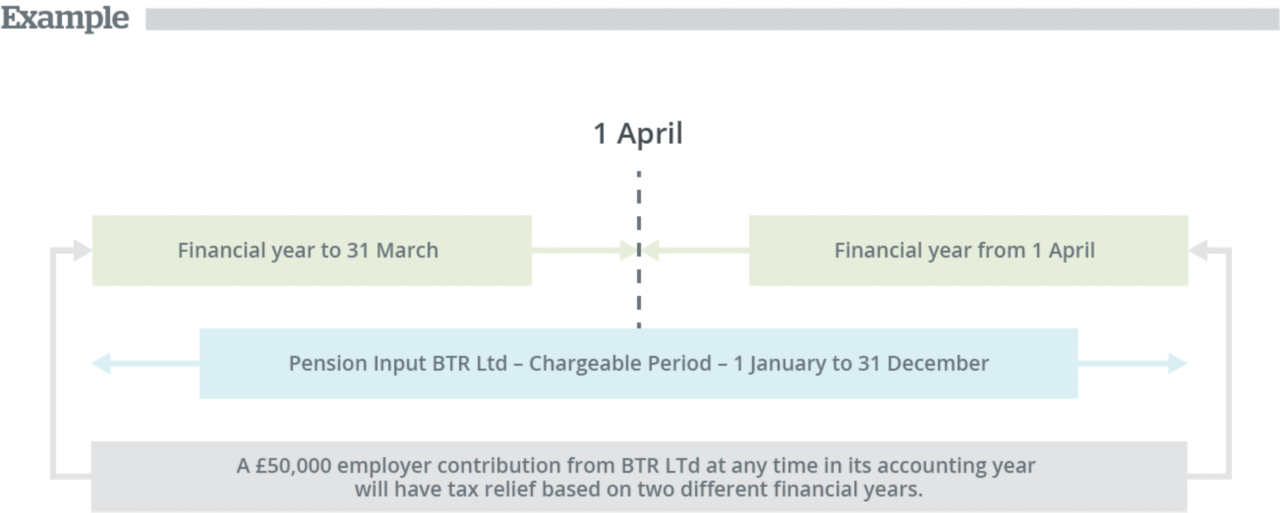

Example

BTR Ltd has an accounting year linked to the calendar year.

It pays an employer pension contribution of £50,000 on 7th July.

This will be deducted from its profits for the chargeable period 1 January to 31 December .

The resulting taxable profit will be apportioned across the previous tax year and the current tax year for the purposes of computing the tax liability - this is different to individual contributions which are assessed in the tax year they are actually paid.

PTM043400

However, there may be spreading of tax relief over a number of tax years where the contributions are large. This applies to contributions to all types of schemes.

Finance Act 2004 s196

Spreading of tax relief

Where large contributions are made by employers, sometimes the relief is not totally given based on the chargeable period, but is spread over more than one period. The rules apply to each individual pension scheme an employer pays in to; it doesn’t apply to the aggregate of contributions to all schemes.

There is a four-step process to decide whether spreading of relief is required:

Step 1

Calculate the amount of contributions PAID in the current and previous chargeable periods.

Contributions to pay for:

- cost of living increases to pensions in payment, and

- benefits for future service for members joining the scheme in the current chargeable period are ignored for calculating the current period contributions but those from the previous period are included.

Step 2

Where the lengths of the chargeable periods are different the previous period gets the following factor applied to the contributions in it:

DCCP/DPCP

Where DCCP = number of days in the current chargeable period, and

DPCP = number of days in the previous chargeable period.

Step 3

Compare the current period contributions against the previous period contributions after any adjustment under Step 2.

There is an excess if current is greater than 2.1 times previous.

The excess is the amount in the current period less 1.1 times the amount paid in the previous period.

Step 4

If the excess is £500,000 or more then spreading applies

The amount of spreading depends on the amount of the 'relevant excess'.

'Relevant excess' contributions of:

- £500K or over, but less than £1m - tax relief spread over 2 years

- £1m or over, but less than £2m - tax relief spread over 3 years

- £2m or over - tax relief spread over 4 years.

Once spreading applies it is not removed unless the employer ceases business.

Sometimes certain employer payments are treated as contributions to a scheme if the purpose of the payment is to try and avoid the spreading rules. We don’t cover this here, but you can find out more details from the Pensions Tax Manual page mentioned above.

The legislation is written so that where no contribution was paid in the previous chargeable period, for example if an employer has only just set up a pension scheme, tax relief on contributions in the current chargeable period won’t be spread.

Finance Act 2004 s197 (as amended by the Taxation of Pensions Act 2014)

Salary Sacrifice

Many employer contributions arise from salary sacrifice arrangements as this allows both employee and employer national insurance savings with some employers retaining their national insurance they save and some passing either all or part of their national insurance saving to the member to increase their benefits. More information on Salary Sacrifice is available in our Salary Sacrifice: the facts, and Salary Sacrifice: pension planning ideas articles.

Impact on individuals

There is no liability to income tax as a benefit in kind for the employee if the employer pays the contributions into a registered pension scheme.

Relevant earnings only apply to member contributions or third party contributions treated as member contributions.

While an employer can pay any contribution level, irrespective of the member's earnings, and may get full tax relief on the contribution it is important to remember that an employer contribution is still subject to normal annual allowance rules for pension contributions, so if a member’s annual allowance including available carry forward is exceeded an annual allowance charge may be triggered.

More information on the annual allowance is available in our dedicated article, and our Annual Allowance calculator can help calculate the maximum pension contribution that can be made within an individual’s available annual allowance taking account of carry forward, and where relevant, tapering of the annual allowance.

Tech Matters

Ask an expert

Submit your details and your question and one of your Account Managers will be in touch.