Income invested and remaining in estate

| Surplus income per month | £1,000 |

| Value (if invested) after 10 years* | £155,929 |

| *5% return net of charges, paid monthly in advance | |

| IHT payable on death (where no Nil Rate Band available) |

£62,372 |

Pensions

Last Updated: 6 Apr 25 19 min read

1. Key Points

3. Eligibility and contributions

4. Pension contributions for others

5. Methods of claiming tax relief

8. Other issues

Learn how tax relief for a member operates including eligibility, methods of claiming tax relief and case studies.

Pension contributions can be paid by:

This article relates to how tax relief operates on pension contributions made by individuals or on their behalf by a third party. The tax treatment of employer contributions is covered in our Tax relief on employer contributions.

Tax relief is given on contributions 'paid' during a tax year. They must be a monetary amount and paid for example, by cash, cheque, direct debit etc.

There’s 'no limit' to the amount of contributions that can be paid. There are, however, limits to the amount of tax relief that can be obtained on those contributions.

This article deals with UK tax relief.

Scottish taxpayers will pay the Scottish rate of income tax (SRIT) on non-savings and non-dividend (NSND) income. NSND income includes employment income, profits from self-employment (including sole trades and partnerships), rental profits, and pension income (including the state pension). Similarly, from 6 April 2019 Welsh Taxpayers pay the Welsh Rate of Income Tax (CRIT (C for Cymru)) on NSND income.

Other tax and deductions such as Corporation Tax, dividends, savings income and National Insurance Contributions etc. will remain based on UK rules. This could mean the amount of income tax relief which can be claimed on pension contributions by Scottish and UK tax payers may not be the same. For more info on SRIT and how this works in practice, please visit our facts page. For more info on CRIT and how this works in practice, please visit our facts page.

Tax relief is available on pension contributions paid by or on behalf of an individual, who is under age 75, if he or she is a 'relevant UK individual'. A ‘relevant UK individual’ must meet one of the following conditions so will qualify if they:

No tax relief is available on contributions paid by or on behalf of individuals who are not ‘relevant UK individuals’.

For tax relief purposes personal contributions include both those paid by the individual member and those paid by a third party for that individual member.

If a self-employed individual makes a pension contribution for themselves, this is treated for tax purposes in the same way as any other personal contribution.

Tax relief is given to the individual – not the third party – and is calculated based on the individual's circumstances. For example, if a parent or guardian pays a contribution for their adult child, the amount payable and tax relief will be calculated based on the adult child's income/earnings.

For clarity, salary sacrifice - a formal contract where the employee swaps some salary for an employer pension contribution instead – will lead to a reduction in the personal tax bill. This is because the employee doesn’t receive the amount of salary given up and, therefore, won’t pay tax or National Insurance contributions on that amount.

The levels of tax relief available depend on the member's relevant UK earnings in the current tax year.

These are the earnings available to base a pension contribution on. Generally, all earned income is relevant earnings.

It’s sometimes easier to think about what are not relevant earnings and this includes pension income, dividends and most rental income.

HMRC define relevant earnings as:

For full information see PTM044100.

If the client receives a redundancy payment the first £30,000 is normally tax free and as such doesn’t qualify as relevant earnings. For example, if the client receives a redundancy payment of £120,000 the amount of relevant earnings is normally £90,000.

For self-employed individuals, historically their relevant earnings were profits calculated over their chosen period of account. These did not need to align with the tax year i.e. 6th April to 5th April, now they have to align to tax years. We’ll cover the changes in detail later.

Where relevant UK earnings are not taxable in the UK due to double taxation agreements they are not relevant earnings.

Not all pension contributions are relievable. The following do not qualify for tax relief for the member;

Prior to 6 April 2024 If a member had relevant UK earnings of less than basic amount of £3,600 but was making a contribution of more than the level of their earnings, relief at source (RAS) was the only method by which the member can get tax relief on the excess contribution (up to £3,600). However, also see below in the net pay section for details on the net pay anomaly.

Historical note: contracted out rebates (minimum contributions) did not qualify for tax relief though there is an element of relief included in the rebate amount.

Transfer values received and pension credit rights received from UK pensions schemes are not contributions.

Transfers of pension credit rights from non-recognised schemes and the transfer of certain shares from ‘save as you earn’ schemes can be treated as contributions and tax relief claimed.

Contributions must be a monetary amount but it is sometimes possible for a monetary amount to be agreed between the member and the scheme and then the member makes good the 'debt' to the scheme by passing over an asset instead. This is known as an 'in specie contribution'

It is not possible to just contribute the asset at whatever its value may be.

There must be:

This is effectively the scheme acquiring an asset.

If the asset is valued at less than the monetary amount the balance must be paid in cash.

Tax relief works as normal based on the monetary amount.

However, HMRC have challenged some of the RAS claims for in specie contributions. In Pensions Scheme Newsletter 86 in April 2017, HMRC stated that their position had not changed and remained as stated in PTM042100 which is described above.

This has been challenged at First and Upper Tier Tax Tribunals and HMRC, and subsequently rejected. So unless there is a further challenge it seems in-specie contributions will not be allowable.

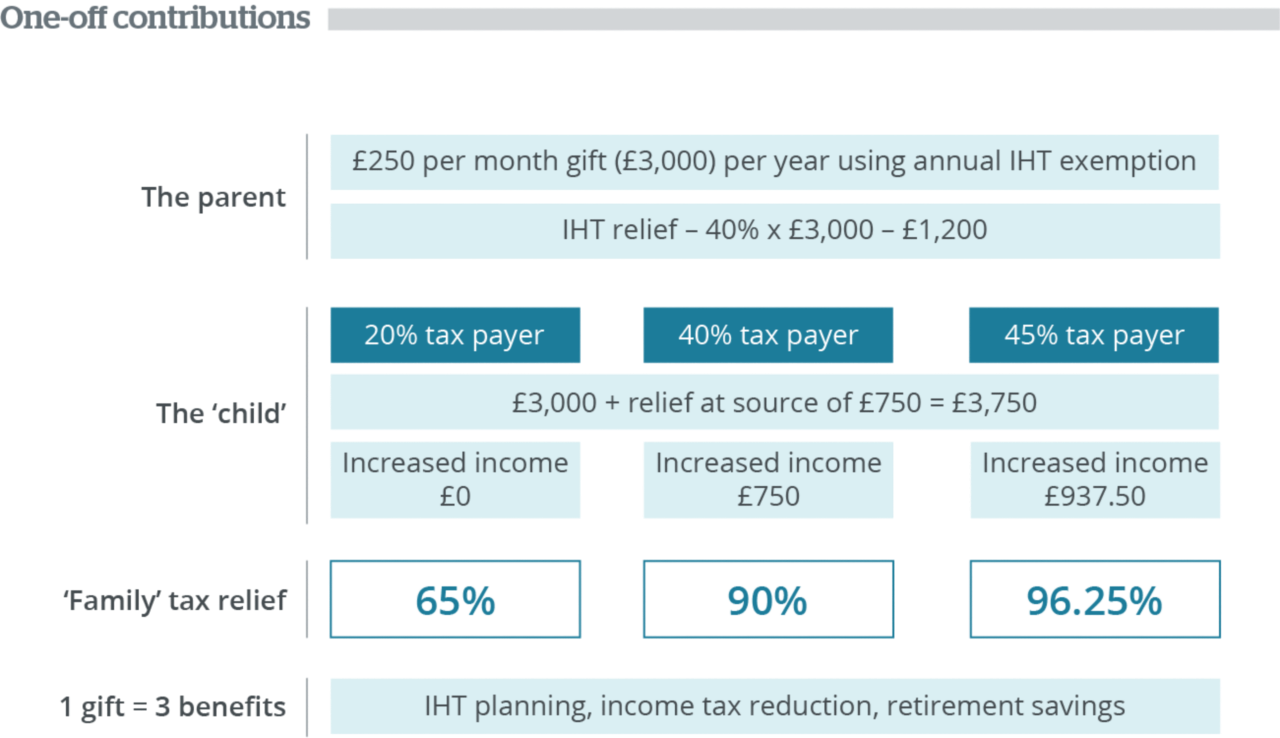

Many inheritance tax (IHT) planning strategies involve making significant capital payments. The objective in doing so is to reduce the taxable estate. A trust is often used to retain control over the ultimate destination and timing of benefits.

One option is to use the tax advantages offered by contributions to registered pension schemes for 'others'.

People mistakenly believe that you will be limited to a contribution of up to £3,600 gross for your children or grandchildren. When the initial reply is followed up by the supplementary question; 'what if that child is in employment and earning £50,000 per year?' the size of the opportunity becomes apparent.

The benefits:

The contribution will be treated as having been made by the scheme member for income tax purposes so will operate as described in our Tax Relief on Member's Contributions article.

Devolved Taxation

Scottish taxpayers will pay the Scottish rate of income tax (SRIT) on non-savings and non-dividend (NSND) income. NSND income includes employment income, profits from self-employment (including sole trades and partnerships), rental profits, and pension income (including the state pension). Similarly, from 6 April 2019 Welsh Taxpayers pay the Welsh Rate of Income Tax (CRIT (C for Cymru)) on NSND income.

Other tax and deductions such as Corporation Tax, dividends, savings income and National Insurance Contributions etc. will remain based on UK rules. This could mean the amount of income tax relief which can be claimed on pension contributions by Scottish and UK tax payers may not be the same. For more info on SRIT and how this works in practice, please visit our facts page. For more info on CRIT and how this works in practice, please visit our facts page.

The IHT treatment will depend on whether the transfer of value (the contribution), is exempt or potentially exempt as described in the IHT articles.

A one-off exempt gift can satisfy multiple planning needs and pass money down the generations tax-efficiently.

The same principles would apply to larger gifts using potentially exempt transfers but death within seven years could reduce or negate the IHT benefits.

Regular contributions can be made using the £3,000 annual exemption available.

Larger regular gifts could be made out of surplus income using the 'normal expenditure out of income exemption'.

| Surplus income per month | £1,000 |

| Value (if invested) after 10 years* | £155,929 |

| *5% return net of charges, paid monthly in advance | |

| IHT payable on death (where no Nil Rate Band available) |

£62,372 |

The 'Child's' Position |

Basic Rate Tax Payer |

Higher Rate Taxpayer |

Additional Rate Taxpayer |

|---|---|---|---|

| Accumulated pension fund | £194,912 | £194,912 | £194,912 |

| Increase in income per annum through tax relief | £0 | £3,000 | £3,750 |

So:

This strategy can also be used if the child is caught in a tax trap, such at the High Income Child Benefit Charge, which can be read in this article.

There are 3 ways to arrange for tax relief on members' contributions:

Used by occupational, employer-sponsored, pension schemes where member's contributions are paid over to the administrator by the sponsoring employer.

Under net pay contributions from individuals are deducted by the individual's employer, from his or her salary before tax is calculated. It’s worth noting that although the pension contribution doesn’t therefore get taxed, National Insurance will still apply on the gross salary.

For example, where an individual wants to pay £1,000 gross the employer would deduct the full amount from salary and pass it to the pension scheme as the individual's £1,000 gross contribution.

In this way, the individual receives tax relief immediately and directly through his or her salary. National Insurance is still payable on the full salary though.

In contrast to net pay, contributions paid under relief at source do not reduce the individual's earnings before tax is calculated. The individual's earnings will be subject to deduction of tax in full.

There has historically been an anomaly for those earning below the personal allowance making contribution under a net pay scheme. They could not obtain any tax relief as they had no taxable earnings. As an example for a member of a net pay scheme earning under the personal allowance it would cost them £100 from take home pay to get £100 in a pension, those using relief at source would only see a £80 deduction from take home pay to get £100 in a pension (as covered below).

From 6 April 2024 there is legislation in place to “fix” this anomaly. HMRC will identify individuals that are affected by this after the end of each tax year and contact the individuals for details to make a payment to them of the equivalent “lost” tax relief in comparison to relief at source schemes. Based on the example above if the individual had paid £100 to a net pay scheme they would get a £20 “refund” to put them in the same position as their relief at source counterparts.

Used by non-occupational pension schemes such as personal pensions, stakeholder pensions and group personal pensions.

Contributions by individuals and third parties are paid net of basic rate tax relief to the scheme and the scheme administrator claims basic rate tax relief from HMRC, which is paid directly into the scheme.

So for every £800 net paid by the individual / 3rd party, HMRC adds £200 to make £1,000 gross.

If the individual is entitled to a rate of tax relief above the basic rate he or she must claim this from HMRC via self-assessment. It’s important to remember that members will only get a rate of relief above basic rate for any taxable income above the basic rate. For instance a member with £1,000 of earnings in the higher rate of tax paying £5,000 gross into a pension scheme operating RAS would only be able to reclaim higher rate relief for the £1,000 that is in the higher rate band of tax.

It can take perhaps up to 10 weeks for the provider to receive the basic rate tax relief from HMRC. However, many schemes / providers will usually gross up the contribution immediately at the time the net contribution is received.

A claim must be made to HMRC:

*Please note that for members with no taxable earnings (i.e. within the personal allowance) no further claim can be made to the revenue, the only way to obtain tax relief for these members would be a payment to a relief at source scheme.

Tax relief is available on the following contributions:

The £3,600 amount is known as the 'basic amount' and only works in a scheme that applies relief at source.

Anyone under 75 can benefit from basic rate tax relief on some or all of the contributions they pay, regardless of whether or not an individual actually pays any income tax.

Where an individual is restricted to tax relief on £3,600 – either because they are non-UK resident or have earnings below £3,600 – they will be able to receive basic rate tax relief in full on the gross contribution only if the pension scheme operates relief at source.

Higher and additional rate taxpayers are entitled to tax relief at their highest marginal rate of tax. This does not necessarily mean that an individual will receive higher or additional rate tax relief on the whole of the contribution.

The tax relief is limited by the amount of an individual's income that falls within the higher or additional rate tax bracket.

For schemes operating relief at source, the additional tax relief is given by extending the basic and higher rate tax bands by the amount of the gross pension contribution (ie the individual's net contribution plus the basic rate tax relief paid to the scheme by HMRC).

The thresholds may only be extended by up to 100% of the members relevant earnings.

Example 1 – client lives in England

Under relief at source or net pay, the overall tax position would be:

In this scenario, the impact of the pension contribution is that it removes the member from the additional rate band.

Example 2

Under relief at source or net pay the overall tax position would be:

In this scenario, the impact of the pension contribution is that it removes the member from the higher rate band.

As mentioned earlier, for self-employed individuals, historically their relevant earnings were profits calculated over their chosen period of account. These did not need to align with the tax year i.e. 6th April to 5th April. However, with effect from 6 April 2024 profits will be taxable in the tax year in which they arise. With 2023/24 being a transitional year to facilitate this change.

Full details of how this basis period reform will operate can be found in our The seven steps required to calculate an individual’s income tax liability article.

These are covered fully in our Annual Allowance, Money Purchase Annual Allowance (MPAA) and Tapered Annual Allowance (TAA) articles. Although the annual allowance rules don’t directly impact on the tax relief given on pension contributions, they do impact on the effective rate of tax relief by the application of an annual allowance charge. Tax relief is given in full and claimed on the self-assessment in the usual manner. However, where the annual allowance (or MPAA/ TAA) is breached there will be a separate charge which will clawback some of the relief gained.

Where an individual mistakenly contributes more than 100% of earnings or £3,600, (if relevant earnings are lower), for example a self-employed person who cannot be sure of their total profits for the year, it is possible to claim a refund of contributions paid that were not eligible for tax relief – ie the excess over the greater of 100% of earnings and £3,600. The rules of the scheme will determine whether the refund is allowed or not, as a minimum the overclaimed relief at source will need to be returned to HMRC.

The individual can claim a refund within six years of the end of the tax year in which the contributions were made.

The refund is called a refund of excess contributions lump sum.

PTM045000

Where an individual or an employer makes a payment to a pension scheme that is returned to them, it may constitute an unauthorised payment.

An error payment is a payment that the scheme has no right to hold and is therefore neither an authorised payment nor an unauthorised payment, ie it’s not a pension contribution within the meaning of the Taxes Acts / Finance Act.

In this case, the error payment (gross) may be returned to the employer without it being treated as an unauthorised payment. The following are examples of valid error payments given by HMRC:

If the employer has obtained tax relief to which it is not entitled to receive, they must rectify this.

HMRC also allow a refund of contributions where membership of a policy / scheme has been cancelled within the 'cooling off' period specified by the appropriate regulatory body. In this case, prior approval from HMRC is not required.

Finance Act 2004 -

Section 188 (Relief for contributions)

Section 189 (Relevant UK Individual)

Section 190 (Annual limit for relief)

Section 191 (Methods of giving relief)

Section 192 (Relief at source)

Section 193 (Relief under net pay arrangements)

Section 166 & Paragraph 6 Schedule 29 (Refund of excess contributions lump sum)

Submit your details and your question and one of your Account Managers will be in touch.